Despite early 2020 concerns that Covid-19 would negatively impact the mobile infrastructure market, through first three quarters of the year the market appears to be on the cusp of a very strong year with nearly 8 percent revenue growth over 2019, according to Omdia.

5G has been the big story of 2020 with most of that taking place in China. In just a little over two years Omdia forecasts 5G RAN revenues will surpass LTE RAN revenues. In comparison it took LTE around six years for LTE RAN revenues to surpass WCDMA RAN revenues. China early and aggressive adoption of 5G has played a big role in this with China accounting for around 65 percent of all 5G mobile infrastructure spend through first three quarters of 2020.

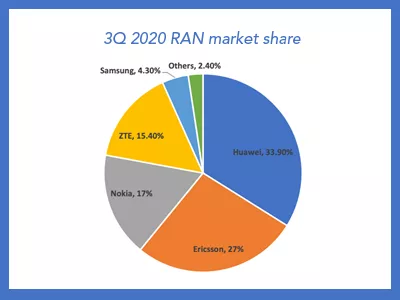

With China’s influence on the 2020 RAN market it is no surprise that its domestic vendors had a strong 3Q. Huawei market share was greater than one-third of the entire 3Q market, giving the vendor the largest share for the quarter. Ericsson had the second largest share, although about 8 percent points less than Huawei. Nokia was third largest vendor by revenue followed by ZTE, although the difference between the two was less than two percentage points. For 5G market share, however, ZTE had the second largest share for the quarter. Huawei had the largest 5G market share with Ericsson coming in a close third behind ZTE.

The other big 2020 story remains Open RAN. While still accounting for less than 1 percent of total market, it is on pace to grow over 250 percent in 2020 versus 2019. Rakuten of Japan is a big contributor to this growth, but there are other areas to watch. Dish Network should start deploying its own Open RAN network in 2021 which will further grow the market. By 2024 with deployments from both greenfield and brownfield operators, Omdia forecast Open RAN will account for over 9 percent of the total RAN market.

Daryl Schoolar, practice leader at Omdia, commented, “5G has given the base station vendors a good 2020. Year over year revenue growth should be one of the strongest in over half a decade. Of course, this success has not been spread evenly between all vendor and markets. The stronger the vendor is in China’s 5G RAN market the better its year. It is remarkable that in around two years, even with Covid-19, 5G will overtake LTE in terms of base station investments.”

While currently the Open RAN market represents less than a single percentage point of the entire market, it will grow in importance during the coming years. This can have a significant impact on the makeup of the market.

Vendors who ignore this trend risk loss of market share that can negatively impact them in the later part of the 5G network era and even into the 6G era. Vendors need to decide how to respond. Do they embrace Open RAN or do they fight it by providing operators with compelling reasons to shy away from Open RAN?