The macroeconomic challenges posed by the conflict in Ukraine, the Chinese property sector crisis, European energy prices and subsequent global inflationary pressures have served to dampen consumer confidence as disposable income dries up. This has resulted in semiconductor demand from smartphones, data centers and consumer electronics floundering. The automotive sector has to date been relatively resilient and consequently, automotive semiconductor demand is bucking the trend. The TechInsights “Automotive Semiconductor Demand Outlook 2021 to 2030” forecasts continued growth with the global automotive semiconductor market serving as a growth engine for the overall semiconductor industry.1

AUTOMOTIVE SEMICONDUCTOR DEMAND OUTLOOK

In 2022, the global demand for automotive semiconductors based on original equipment manufacturer (OEM) vehicle production grew by 24 percent year-on-year to reach $54 billion, averaged across all applications, including sensors. A combination of strong demand and constrained supply translated into semiconductor pricing increases which also served to further bolster revenues for the automotive semiconductor industry. In 2023, the automotive semiconductor market is forecast to grow by 19 percent and the referenced report forecasts that the global automotive semiconductor market will almost triple by 2030.

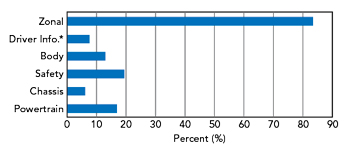

Figure 1 Automotive semiconductor growth by domain. Source: TechInsights forecast.

This revenue increase is not being driven by a tripling of vehicle output. Instead, it is the semiconductor content per vehicle that is increasing over this timeframe. This is reflected by growth trends across the vehicle domains of powertrain, body, chassis, safety and driver infotainment, as well as the emergence of a zonal domain. The semiconductor growth rate performance for these domains is shown in Figure 1.

Underpinning this growth will be the continued momentum towards electrification. Electrification, in turn, is a core tenet as the automotive industry moves towards domain-based and zonal electrical/electronic (E/E) architectures. The goal is to enable vehicle capabilities across advanced driver assistance systems (ADAS) and automated driving (AD), along with advanced infotainment, telematics and vehicle connectivity.

Growth of the “zonal” domain will be predicated upon the move towards new platforms that will be underpinned by battery electric vehicles. Semiconductor demand from zonal controllers will grow at a compounded average annual growth rate (CAAGR) of 83.5 percent from 2022 to 2027. This demand will account for an additional $84.7 billion of cumulative demand from 2022 to 2030, as it drives up the use of increasingly sophisticated semiconductor processors to support the push toward a software-defined vehicle (SDV).

The continued expansion of OEM electric vehicle (xEV) offerings is driving high levels of semiconductor growth, particularly for power electronics and battery management components within the powertrain domain. The powertrain domain is forecast to grow with a CAAGR of 18 percent from 2022 to 2027. As outlined in the TechInsights “xEV Semiconductor Demand Outlook 2021-2030,”2 xEV light vehicle powertrain production, incorporating mild hybrid, full hybrid, plug-in hybrid and battery electric vehicles, will grow from 21 million units in 2022 to reach 58 million units by 2030. The push to electrified powertrains is being dictated by consumer awareness and government regulations and mandates related to climate change and the need to reduce emissions and slow the impacts of global warming. With timelines ranging from 2030 to 2040, several countries have put into play policies that effectively ban the sales of internal combustion engine-based vehicles.

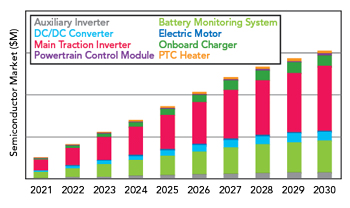

Figure 2 xEV powertrain semiconductor demand. Source: TechInsights.

The corresponding xEV powertrain semiconductor demand from battery management systems, DC/DC converters, main traction inverter, electric motor and onboard charger and other systems is forecast to grow at a CAAGR of 24 percent, reaching $31 billion by 2030. The system segmentation for the total semiconductor revenue in xEV powertrains is shown in Figure 2. Battery electric vehicles will comprise the largest market for semiconductors growing at a CAAGR of 31 percent and accounting for 86 percent of the total xEV powertrain semiconductor market opportunity in 2030. The move to battery electric vehicles will be accompanied by a push towards increasing use of wide bandgap technologies. By 2030, the industry will be approaching a tipping point when silicon carbide (SiC) semiconductor demand starts to exceed that of silicon power semiconductors. There will also be an emerging opportunity for GaN power electronics.

While xEV powertrains become mainstream, the number of ADAS/AD sensors per vehicle will continue to grow. This will mean that the safety domain will grow at a faster CAAGR of 21 percent from 2022 to 2027. Safety domain growth is driven by a combination of rapid ADAS adoption in premium and mid-range vehicles, continuing penetration growth of passive safety systems in the emerging markets and the inclusion of additional safety systems to meet safety rating requirements.