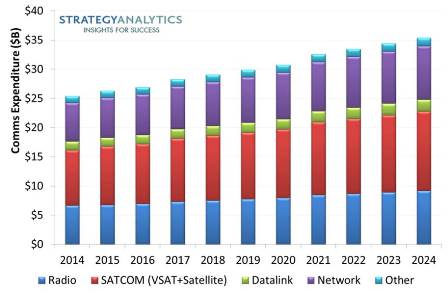

Strategy Analytics defense research has just completed a comprehensive analysis of the military communications sector, looking at radios, communications satellites, VSAT terminals, datalinks, networks and other systems. Trends driving spending on the military communications sector will be underpinned by network-centric IP-based communications that will translate to spending on global military communications systems growing to over $35.3 billion in 2024, representing a CAGR of 3.4%. Summarised in Global Military Communications Market Forecast: 2014 - 2024 and supplemented by a series of forecasts that outline global military communications expenditure trends on a regional basis before breaking out the expected spend across systems, hardware, support and related services with a deeper look at the prospects for military radios and satellite terminals, across the land, air and naval domains.

Some of the top level trends and observations include:

Some of the top level trends and observations include:

- North America will be the largest regional end market, but will be superseded from 2016 onwards by demand from the Asia-Pacific region.

- Land-based communications will represent the largest market both in dollar terms as well as in terms of total shipments.

- In terms of systems, spending in the military communications sector will be dominated by satellite communications, comprising space-based satellite systems as well as the ground-based satellite terminals, with a a steady launch schedule for military communications satellites over the forecast timeframe.

- An increasing emphasis on IP-centric communications that support data as well as voice communications will be enabled through systems that are also able to operate across multiple modes and bands. This will continue the drive towards communications systems underpinned by enabling technologies that can support broadband performance, higher frequencies and digitization.

The moves towards bringing advanced capabilities will mean there will be continued spending on military radios with the market expected to exceed $9 billion by 2024. Strategy Analytics Global Military Radio Market and Technology Forecast: 2014 - 2024 outlines analysis looking at the total military radio sector providing segmentation detail related to form factors, platforms, frequency, power and associated enabling component demand.

- We expect the Asia-Pacific region will drive spending on tactical radios for especially for land-based communications and account for the largest end market over the entire forecast period.

- Land-based radios will represent the largest market both in dollar terms as well as in terms of total shipments.

- The total number of radio shipments is forecast to grow at a CAGR of 3.5% through 2024 to reach 172,867 units.

- While traditional HF, VHF and UHF radio frequencies will maintain use, there will be an increasing emphasis towards systems that can support multi-band and/or wideband operation and the market for these radio systems will account for 47% of the total global military radio market in 2024.

- Handheld radios will drive the volume in the land-based military radio market, which will grow to $6.5 billion. Smaller platforms such as fast attack craft and offshore patrol vehicles, and the helicopter and light aircraft segment, will drive volumes in the shipborne and airborne segments.

- The associated market for radio component technologies will grow from $710 million to almost $1.1 billion with GaN becoming an established technology as it grows at a CAGR of 32.7%.

There will be continuing demand for satellite communications which will also translate to increased spending on military satellite terminals. Strategy Analytics expects this spending to approach $6 billion in 2024 looking at the total military satellite terminal sector.

- North America is estimated to have the largest demand, but will be superseded by spending from the Asia-Pacific region from 2017 onwards. There will also be growth in demand from the other regions with spending in the MEA region expected to grow at a CAGR of 4.3%.

- Land-based terminals will represent the largest market in dollar terms, accounting for 49% of the total market, and also represent the bulk of volume in terms of total shipments.

- The total number of terminal shipments is forecast to reach over 8000 units, representing a CAGR of 3.8% through 2024. Portable/dismounted terminals will drive volume in the land sector while the airborne sector will start to see increasing demand from the UAS platforms.

- As well as growing demand for higher frequency Ka-band terminals, there will be an increasing emphasis towards systems that can support multi-band and/or wideband operation which will also influence future component technology choice and demand.

- Despite solid-state semiconductor technologies such as GaN seeing increasingly robust adoption, a continued emphasis on high power, long range communications, especially in the shipborne military satellite terminal market, will translate into the market for vacuum tube-based components remaining stable.

We forecast spending on defense systems will approach $140 billion by 2023, translating into a substantial opportunity for component technologies suitable for radar, communications, EW and other military/defense systems.