Each year, the global deployment of 5G-enabled devices and infrastructure expands, with 98 nations having commercialized 5G or conducting 5G trials in 2022, up from 79 nations in 2021. The developing 5G network introduces two new frequency bands, sub-6 GHz (3.5 to 7 GHz) and mmWave (24 to 71 GHz), the latter of which enables extremely low latency and substantial bandwidth (which allows for higher data throughput). With these advancements come new applications, like smart devices, autonomous vehicles and remote medical monitoring, that were impossible to access with previous telecommunication technology.

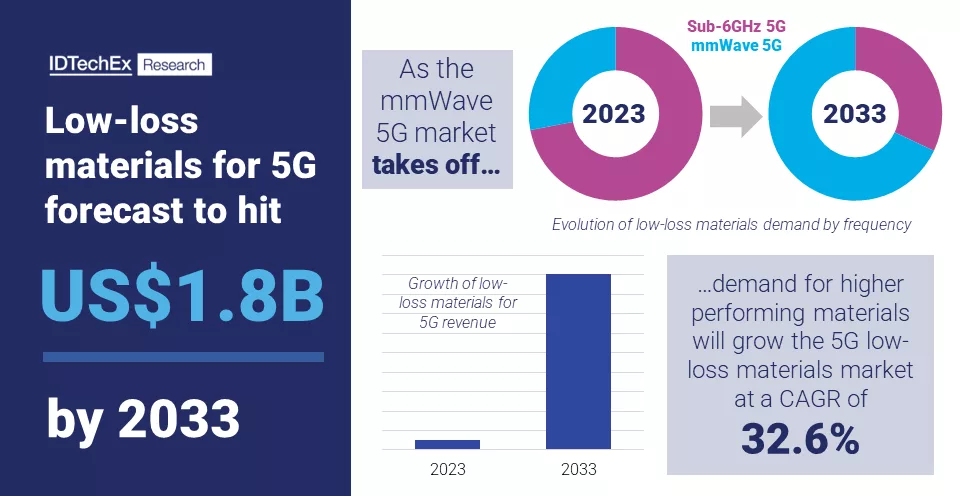

However, the expansion of the 5G network, particularly the higher frequency mmWave bands, is restricted by several challenges. One of these is the high transmission losses of the materials used in 5G infrastructure and devices, which contributes to poor signal propagation. Improving the dielectric properties of these materials, found in every corner of a 5G device from the printed circuit board (PCB) to the antenna to the IC-packaging, is critical to reducing transmission loss and enhancing 5G signal. This need is fueling the rapid growth of the low loss materials market for 5G applications, which IDTechEx forecasts to hit US$1.8 billion by 2033.

Currently, sub-6 GHz applications play a major role in the 5G market as the most deployed 5G frequency band to date. While sub-6 GHz is important for 5G, mmWave is the more exciting 5G frequency band, both from an applications and materials standpoint. While existing popular low loss materials, like epoxy-based FR-4 and BT, are suitable enough for the incremental performance improvements brought by sub-6 GHz, even lower-loss materials are required to address the much higher performance demands of mmWave 5G applications.

This presents more opportunities for materials innovation, as other materials from PI to PTFE to PPE to low temperature cofired ceramic (LTCC) compete to address the low loss needs of mmWave 5G. While organic materials have higher popularity thanks to their lower cost and higher technology maturity, inorganic materials like and glass have garnered significant interest thanks to their favorable dielectric properties and integration abilities, which may pay off in the medium term. However, all these materials have different considerations, including environmental stability, cost, supply chain maturity, manufacturability and more, which will make some more suitable for applications like 5G smartphones and others better for 5G infrastructure. Overall, the takeoff of mmWave 5G-enabled devices like customer premises equipment (CPEs), made possible by these emerging higher-value low loss materials, within the decade will subsequentially fuel the low loss materials market's exponential growth through 2033.

Even though 5G has not been fully deployed, the telecommunications industry is already preparing for the next generation of 6G, whose frequency spectrum is expected to expand into the sub-THz range (100 to 300 GHz). Considering the ever-increasing importance of reduced transmission losses at such high frequencies, academics and materials suppliers are already exploring ultra-low loss materials that could enable 6G. In examining the current development of low loss materials for 6G, IDTechEx noted that the many diverse materials that researchers are taking to tackle 6G applications suggests even more revenue opportunity for the low loss materials market in the long term. While IDTechEx expects the market to grow to USD$1.8 billion in a decade, the industry will likely reach new heights with the future advent of 6G.

Market Forecasts for Low loss Materials for 5G and 6G

IDTechEx's latest report, "Low loss Materials for 5G and 6G 2023-2033," explores the technology developments and market trends driving the growth of the low loss materials market for next-generation telecommunications. IDTechEx forecasts future revenue and area demand for low loss materials for 5G while carefully segmenting the market by frequency (sub-6 GHz vs. mmWave), six material types and three application areas (smartphones, infrastructure and CPEs) to provide sixty different forecast lines.