Smart devices, autonomous driving, remote patient monitoring – countless new applications are being unlocked by advancements in telecommunication technology, specifically the transition to 5G. 5G telecommunications introduces two new frequency bands: sub-6 GHz (3.5 to 7 GHz) and mmWave (24 to 71 GHz). It is mmWave 5G that allows for extremely low latency and substantial bandwidth, thus allowing for higher data throughput, both of which are necessary to enable the new applications previously mentioned. As such, a network of 5G-enabled devices and infrastructure is growing worldwide, especially in important markets like China, leads the global 5G mid-band deployment with over 68 percent of the market share, according to IDTechEx.

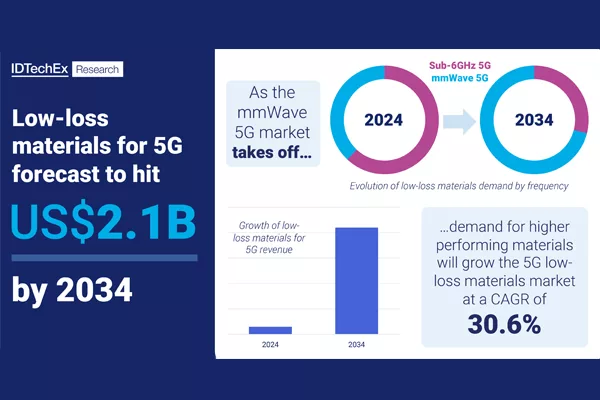

Expanding the global 5G network is not a straightforward task; there are many technical challenges to be overcome, particularly for the higher frequency mmWave bands that are of high interest for many applications. These technical challenges include a key material problem: the high transmission losses of materials used in 5G components such as filters and antennas. High transmission loss leads to poor signal propagation, which would severely limit the efficacy of 5G communications. Reducing this transmission loss is a key task for the advancement of 5G telecommunications, so it is critical to improve the dielectric performance of materials found throughout 5G devices, including the printed circuit board (LCB), antenna, IC-packaging and more. This demand for low transmission loss, or low-loss, materials for 5G applications is buoying the market to surpass USD$2.1 billion by 2034, as predicted by IDTechEx’s new report, “Low-Loss Materials for 5G and 6G 2024-2034: Markets, Trends, Forecasts."

The transition from sub-6 GHz 5G to mmWave 5G to 6G and beyond

As sub-6 GHz 5G is the most deployed 5G frequency band to date, low-loss materials used in sub-6 GHz applications comprise about two-thirds of the 5G market by revenue in 2024, as estimated by IDTechEx. With performance requirements only slightly higher than 4G, sub-6 GHz applications are effectively served by existing low-loss materials such as epoxy-based FR-4 and BT.

However, the performance leap from sub-6 GHz to mmWave 5G demands dielectric materials with even lower dielectric loss than incumbent materials. This is creating opportunities for materials innovation in this market to displace the incumbent materials. Organic materials such as PI, PTFE and PPE offer a balanced mixture of dielectric performance, cost and manufacturability. Meanwhile, inorganic materials like glass and low-temperature cofired ceramic (LTCC) offer the opportunity to create highly integrated and miniaturized components. The strengths of each of these low-loss materials for 5G applications will need to be weighted to ascertain their suitability for key applications like smartphones, customer premises equipment and base stations.

As the deployment of 6G, whose frequency spectrum is expected to include sub-THz bands (100 to 300 GHz), looms, there is continued innovation to explore ultra-low-loss materials to enable this next-generation of telecommunications. IDTechEx extensively explores all these different approaches in low-loss materials for 5G and 6G in their new report, “Low-Loss Materials for 5G and 6G 2024-2034: Markets, Trends, Forecasts,” to understand how innovation will enable the industry to grow exponentially in market size by 2034.

Market forecasts for low-loss materials for 5G and 6G

IDTechEx’s latest report, “Low-Loss Materials for 5G and 6G 2024-2034: Markets, Trends, Forecasts,” explores the technology developments and market trends driving the growth of the low-loss materials market for next-generation telecommunications. IDTechEx forecasts future revenue and area demand for low-loss materials for 5G while carefully segmenting the market by frequency (sub-6 GHz versus mmWave), six material types, and three application areas (smartphones, infrastructure, and CPEs) to provide 60 different forecast lines.