The Qualcomm RF360 envelope tracking power supply hit production during the past couple of months, in the Samsung Galaxy Note 3. The funny part was that it is not attached to the Qualcomm CMOS power amplifier. Instead, the Qualcomm Power Management IC drives a GaAs PA supplied by Avago.

To old radio guys like me, the rise of CMOS power amplifiers brings back memories of the first integrated CMOS transceivers for mobile handsets. Back in the 1980s, with AMPS cellular systems, the handset used discrete components in the transceiver. By the 1990s, when 2G systems were starting to ramp up, baseband modem suppliers suggested a migration to CMOS transceivers.

In 1993, many RF engineers laughed at the idea of an integrated CMOS transceiver. Comments like “You’re going to sacrifice sensitivity” or “you won’t get enough linearity in your front end” were common. But here we are. Twenty years later, it is impossible to find a discrete handset transceiver anywhere in the world.

It is true that the systems engineers sacrificed noise figure and linearity and a few other metrics to achieve the flexibility and low cost of CMOS transceivers. But the benefits of 2G standards (coding gain for CDMA, or wider FM bandwidth for GSM) made up for these sacrifices and it worked out okay.

We will see the sequel to this movie with CMOS power amplifiers. We have seen CMOS PAs take over the constant-envelope GSM market, at price levels that GaAs products will not match. A few 3G handsets now include CMOS PAs, and the battle has begun.

Technical Comparison

There’s no doubt that GaAs performs better. As Peter Gammel illustrated in the August issue of Microwave Journal, GaAs has a performance advantage in both efficiency and linearity, resulting in roughly 10 percentage points better efficiency with other factors held constant. Especially for waveforms with a high peak-to-average ratio, the combination of power, linearity and efficiency is inherently better due to physical attributes of the semiconductor material.

Recently, mobile terminals have started to use multi-mode, multi-band power amplifiers (MMPA) which cover a much wider operating bandwidth than single-band PAs. This is just one more design constraint that limits efficiency/linearity improvement for both CMOS and GaAs.

To continue the improvement, almost all PA suppliers and handset OEMs are investigating envelope tracking (ET). Put simply, ET involves a fast power supply that ramps the voltage rail for the amplifier along with the modulated waveform. As peak power requirements spike up, the supply voltage ramps up. The idea here is to only provide the power that is necessary at any instant in time. CMOS amplifiers are now emerging that use ET to achieve performance roughly on par with non-ET GaAs amplifiers. At the same time, GaAs amplifiers with ET provide excellent efficiency performance. The Samsung Galaxy Note 3, launched during September, uses a Qualcomm ET power supply, with a GaAs PA from Avago in order to achieve a longer battery life.

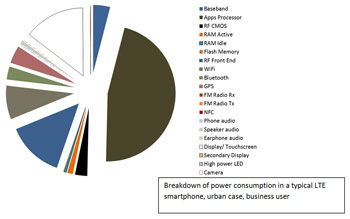

Figure 1 Breakdown of power consumption in a typical LTE smartphone, urban case, business user.

Performance That is “Good Enough”

Better performance is always desirable. But at some point, performance for a PA can be “good enough” for a segment of the market. We have seen that already for the GSM market, where CMOS has taken over despite performance tradeoffs. With the arrival of ET, several modem suppliers are betting that CMOS is now “good enough” for some 3G and LTE applications.

From a cost point of view, CMOS PAs are generally perceived as lower cost. Are they? This question has been largely theoretical for several years, but during the past six months, the idea has been subjected to a real-world test. RFMD acquired Amalfi Semiconductor in November 2012 and found that initially the manufacturing cost was too high. However, with a redesign of the CMOS PA to utilize RFMD’s streamlined assembly and test facilities, the RFMD CMOS PA will achieve a cost far lower than previous GaAs products. Extending this to 3G and 4G products will take more work, but one initial proof-of-concept is now established.

How Important is a 10 Percent Advantage in PA Efficiency?

Battery life is important to mobile operators, but as multi-core apps processors and large displays have taken over the smartphone market, the RF section of the handset consumes less of the total power. In the Mobile Experts Battery Life Model, the RF front end represents between 14 and 20 percent of the power consumed in a smartphone, accounting for the typical distribution of LTE transmit power levels in an urban network and the losses of a complex multi-band RF front end (see Figure 1). That means that 10 percentage points in PA efficiency results in about four percent longer battery lifetime for a heavy smartphone user, or about half an hour.

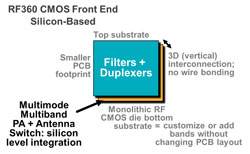

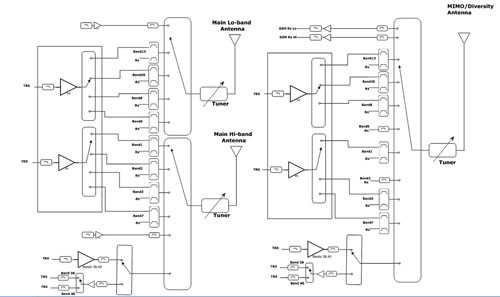

Figure 2 Qualcomm RF360 CMOS RF front end module.

In the high-end smartphone market, half an hour is still a worthwhile level of differentiation, so Mobile Experts forecasts that these markets will use GaAs for quite some time. With simpler 3G handsets in cost-sensitive markets, the cost/benefit decision is not yet clear.

RF Integration

A Complete Front End (CFE) – like Qualcomm’s RF360 (see Figure 2) or the Skyworks SkyOne product line (see Figure 3) – represents a single module which addresses all of the RF devices between the transceiver and the antenna. The power amplifiers, filters and duplexers, switches, and antenna mismatch tuning can all be included in the module. This makes life easy for the customer, and in some cases the CFE can save space in the handset. As a result, the CFE is likely to capture a significant portion of the handset market.

On the other hand, the high end of the market is unlikely to benefit much from the CFE. The latest iPhone 5s and the Galaxy S4 are very complex, customized products. Integrating everything into a single module (and concentrating production with a single vendor) increases risk and time to market for the major smartphone vendors.

Figure 3 Skyworks SkyOneTM system in package.

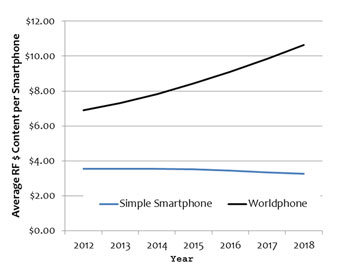

Figure 4 Average dollar content for RF per smartphone.

From an RF vendor’s point of view, the investment of R&D resources into any RF project is a bet that the resulting product will be useful. A multidisciplinary CFE project can cost $10M or more in R&D expense. No single handset product achieves enough volume to make the R&D cost worthwhile. Because of the straightforward economics of return on investment, any semiconductor vendor will focus CFE development on the most common mainstream applications. The ROI decision can be illustrated with two case studies:

Economics of an Entry Level 3G Smartphone

A CMOS-based CFE with integrated duplexers and filters, covering quad-band GSM and a single 3G band would be useful in at least 40 different handset models. This kind of simple CFE could reach a volume of 100 million units per year, with a long product life cycle. The R&D investment of about $10M would be amortized over 300 million units, reducing the cost burden to three cents per unit.

Of the 2.2 billion handsets produced this year, 1.7 billion are feature phones, simple smartphones with three data bands or fewer, PC dongles, tablets or M2M modems. Most of the industry focus falls on the high-end smartphones, because smartphones with four or more data bands (worldphones) are the most complex and challenging applications. Today, 84 percent of handsets have three or fewer data bands. CMOS-based CFEs are targeted at this market (don’t listen to all the hype to the contrary). Mobile Experts predicts that the RF dollar content in an entry-level smartphone will decline over the next few years (see Figure 4).

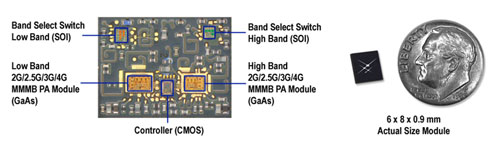

Figure 5 An example of the level of customization in a multi-band "worldphone."

Economics of a Single-SKU “Worldphone”

A CFE covering 12 different data bands (plus quad-band GSM) represents a much higher level of R&D investment, with a complex filter bank and a multi-mode multi-band amplifier in addition to switching and possible antenna tuning (see Figure 5). Creating this kind of CFE module could cost $40M or more in R&D expense. Then, the production run would last for about 12 to 18 months before the product would be replaced by something else. Even with a successful run of 100 million units, the R&D cost represents 40 cents per unit, not three cents.

Another issue comes from time-to-market. Our hypothetical single-SKU super-module would be difficult to develop in the right bands, power levels and form factor within the R&D cycle. Samsung and Apple do not know exactly what they need two years from now.

In general, handset OEMs do not pay premium prices for integration. A PA/duplexer module does not sell for a higher price than the discrete PA and duplexer separately. While the CFE saves R&D cost for the OEM, our estimated 40 cents in R&D cost cannot be passed along to the OEM as a higher price.

Looking at the worldphone market, the growth is clear. The iPhone’s entry into China will result in big growth for worldphones. By 2018, 42 percent of the handsets produced worldwide will include four or more data bands. With far higher dollar content than entry-level smartphones for RF devices, there is still major growth in the high end of the RF front end market.

Market Segmentation

When Henry Ford built cars and trucks in the 1910s, he put the same transmission into both vehicles. The early automotive market fit this model of commonality, and mass-producing a single transmission drove improvements in quality and cost that made vehicles affordable for everyone. Eventually, the market grew large enough that investment in different transmissions for lighter cars and heavy trucks made economic sense.

The mobile terminal market has finished that early phase of market development, where the same modular strategy was used for every application. At $5B in market size, the mobile RF front end ecosystem can support different product strategies for different tiers of the market. The CFE approach is most viable for the RF suppliers at the low end of the market, where R&D investment is lower and volumes are higher. A modem supplier like Intel or Qualcomm can offer a CFE for low end smartphones and capture a sizable chunk of market revenue. At the high end of the market, separate modules used in more flexible combinations are a better solution.

It’s About the Processors

While the PA engineers arm wrestle over which wafer to use, another fight is taking place in the modem. Qualcomm has lost significant market share to MediaTek and Spreadtrum in China, and it wants it back. One way to do that is to offer a simpler product line, with a chipset that takes care of everything: applications processor, modem, transceiver and RF all the way to the antenna. A handset OEM does not need deep RF expertise with this approach. Enter Qualcomm’s RF360 product, which includes the ET power supply, PA, filters and antenna tuning. For entry-level smartphones, this addition to the Qualcomm product line could make it easier to sell modems.

Intel, Mediatek, Broadcom, Nvidia, Spreadtrum and Marvell are all working on ET programs, indicating that there is some merit to this strategy for processors. At this moment, there is only one modem supplier with an ET/PA product – but as time passes, multiple competitors will take part and the modem/transceiver/ET/PA relationships will become very important in the market. Some of these vendors plan to use CMOS PAs, and others have GaAs partners.

By themselves, Qualcomm will not compete aggressively for PA business. (A great example is the Galaxy Note 3, where Qualcomm is happy to support a GaAs PA). Things will change when Qualcomm, Intel and MediaTek begin to compete head-to-head with solutions that include RF. Fighting for the bigger modem business, the price erosion in PAs may be severe. These companies may need to defend their modem business with low prices for PAs. It is never healthy to add a few new competitors into a market which is below about 10 percent growth.

Market Impact

For GaAs vendors, the main question comes down to this: How much market share will CMOS take? Will the GaAs fabs be fully utilized? Will price erosion become a problem?

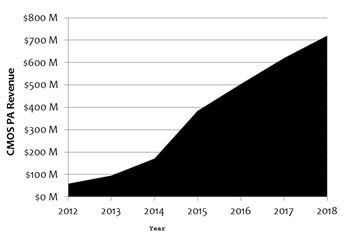

Figure 6 CMOS PA revenue projection.

The market for GaAs power amplifiers was already slowing, as multi-mode, multi-band PAs take hold and limit market growth by reducing the need for additional PAs in new bands. In the Mobile Experts forecast “RF Front Ends for Mobile Terminals 2013,” overall RF front end market revenue will grow by 15 percent annually for the next five years, but the PA segment growth will be much weaker, at six percent or possibly lower due to a combination of MMPA adoption and price erosion.

In the 1990s, the battle between discretes and CMOS transceivers was short and decisive. The sequel will not end the same way. In the PA world, changing peak-to-average requirements play directly into the strengths of GaAs. Fragmented frequency bands mean that most worldphones will need to be highly customized for years to come. There is no clear path for CMOS to enter the high end of the market, where performance matters.

Emerging CMOS products will gobble up the low end of the market, growing to more than $700M by 2018, or roughly 25 percent of the total PA market value (see Figure 6). GaAs PAs will continue to dominate the high end. In the end, the CMOS PA growth will rob the GaAs PA suppliers of the opportunity for market growth, and the “cash cow” business at companies such as RFMD and Skyworks will be impaired. A few GaAs suppliers will continue to succeed, but they will compete for a flat GaAs market in a highly fragmented LTE landscape. Nobody ever promised that life would be easy.

Joe Madden founded Mobile Experts in 2002, and serves as the company’s primary expert in semiconductors for handsets and infrastructure. A Silicon Valley veteran, Madden has 24 years of experience in wireless hardware, supplying amplifiers and filters into both base station and handset applications. He survived two startups, including successful IPOs and LBOs along the way. He holds a degree, cum laude, in Physics from UCLA.