Whatever your perspective, be that from the position of a small operator who hopes to gain a market advantage, or of a large incumbent supplier or network operator, the fundamental question about WiMAX is whether it can ramp to volumes that enable it to compete in a world ruled by huge volumes of cell phone sales. WiMAX and future wireless networks that aspire to 4G will attempt to become unified communications systems that fit diverse markets that have very different sets of customers and requirements. The common architecture is supposed to result in overall advance in technology and reduction in costs: the ‘virtuous circle’ enabled by a large symbiotic ecosystem.

How Does WiMAX Build to a ‘Tipping Point’?

A buzzword that has filtered through discussions of WiMAX has been that a nexus of contributing factors would be assembled that leads to a ‘tipping point’ at which WiMAX momentum skyrockets. The many pieces to the puzzle include:

• Gaining availability to sufficient spectrum for wide-area coverage and roaming

• Assembling large numbers of component, core systems, and device suppliers and ODMs to fuel creative development and provide users with options for diverse markets.

• Foster an IPR environment that lowers the barriers and risks.

• Create an open system that leverages developments in other industries including Internet, PC and server software, network systems and OS, service industries including voice phone, entertainment, advertising, and unified messaging services.

• Leverage market momentum and pent up market demand from broadband networking, computing, and cellular phone markets.

Many parts of the puzzle must develop as groundbreaking efforts that occur over a period of years. Standards, regulation of spectrum and licensing, development of WiMAX ICs and systems, these all take time to develop before they become enabling of a tipping point to mass market adoption.

But at some point we start looking for the market developments that ignite the tinder and set off the blaze of cascading adoption.

The market has welcomed the announcement of Sprint and Clearwire as potentially igniting development and market growth. Prior to that important announcement, many thought that the large under-served markets of India, China, Indonesia plus many other contributing regions would be where growth would likely spring. The differences between the highly developed market of Sprint and a digital inclusion market like India are almost polar opposites: Sprint must deliver products, coverage and mobility that are competitive with mobile data phones, DSL and cable and packaged services. Products can include very rich media devices and laptops that command high ASPs. The emerging markets must provide very low cost connectivity. While the competition is much less, there is difficulty in delivering the required ASPs.

Regardless of whether developed or emerging propel volume markets; the tipping point still comes into play. Most of the WiMAX chip, antenna component, RFIC suppliers either are fabless or use automated manufacturing methods so that price scales down rapidly with volume. Many of the parts can be used across multiple spectrum bands and applications. To give some examples:

• Several WiMAX chip suppliers indicate that price is highly volume elastic: one fabless Asian supplier that is designed into a few devices we know of say that WiMAX modem pricing is expected to reach $5 or less within two years as volume per year scales over 1 million pieces. Other manufacturers were reluctant to provide exact targets but agreed that the emerging markets they targeted would require BOM pricing to enable sub $120 CPEs.

• WiMAX antenna with experience in cellular handset markets have provided component designs and pricing guidance that supports construction of the necessary emerging market BOM pricing.

We have seen that the tipping point, however reached, is volume.

Sprint-Nextel, Clearwire and other common 2.3-2.6 GHz deployments have dimmed somewhat as the catalyst for WiMAX during 2008. Market troubles due customer attrition from old networks and other service issues has put Sprint-Nextel more in the defensive mode. While they remain optimistic about the future of WiMAX, the immediate push is dependent on certifications, product availability and market demand.

But as the enthusiasm for market leading deployments by Sprint have somewhat dimmed, the enthusiasm for adoption in under-served markets in India and elsewhere have turned:

The recent announcement of deployments in emerging markets may be the added nudge WiMAX needs to reach the tipping point.

Three recent announcements add fuel to the fire of emerging market deployments: BSNL, India, Wateen, Pakistan (extended deployments), and Packet One Networks, Malaysia. What is particularly significant is that the high volume emerging market deployments aggressively push down the unit pricing for SUs, particularly for DSL replace class CPEs.

State owned BSNL, the largest telecommunications company in India, is the current prospect to achieve the highest volume WiMAX base station and CPE deployments in emerging markets. Due to that, BSNL was able to acquire nationwide coverage of 2.5 GHz spectrum which some think is the best compromise of frequencies for use as wireless personal broadband because it can deliver a favorable trade-off between high bandwidth and long range. The company says that they now have a wide enough band to deploy WiMAX triple-play services including voice, video, and Internet access. BSNL has provided triple-play over broadband in pilot cities and has gone out for additional tenders to extend the network as their broadband service area is expanded.

BSNL plans to roll out WiMAX services in 70 cities across the country by mid-2008 and set up 50,000 Common Service Centers (CSCs) across the country using WiMAX under the Indian government’s "Vision 2010" mandate to extend broadband services to 20 million people by 2010. Although this can include DSL and fiber optic, the majority of subscribers are expected to be connected by WiMAX and Wi-Fi.

Yatish Pathak, Soma Networks CEO, told us that BSNL was able to build out extensive fiber optic networks in what is called FTTN, fiber to the node. Yatish said that this could not have been done to the same extent in many countries. Due to being a state owned utility, BSNL has been able to gain the funding and authority to build out a nationwide gird of fiber that provides a perfect back-haul for WiMAX and other broadband communications. Maravedis has advocated that municipalities in Europe, America and other regions similarly build out FTTN to serve as facilitator for public and commercial broadband. BSNL and other telcos in India have built out an enviable network of FTTN.

In many parts of the world extending and increasing back-haul grid networks is a major obstacle for rapid and cost effective deployment of broadband. Sprint and other operators face the difficulty of building back haul in a hodgepodge of government jurisdictions.

According to BSNL the deployments will be staged. In the first phase under the tie-up, WiMAX will be deployed in Ahmedabad which would be up and running by June-July this year according to India’s Economic Times publication. The deployments are expected to cover 250 people and will take three years. Deployments may be further extended, according to BSNL, to cover about 500 million citizens. BSNL CMD, Kuldeep Goyal told the Economic Times that “BSNL has awarded the contract to Soma for complete deployment in these states. It’s difficult to put a value to the contract since it’s on a revenue-share basis.”

While the alliance between India’s largest telecom operator and Soma Networks is on a revenue-share basis that makes it difficult to calculate the full size and scope of the award, the numbers of the initial phase and price objectives for CPEs provide enough information to consider the broader implications. Yatish Pathak said that the price of CPEs is targeted at $100 and that they were confident they can meet the needed objectives using their current contract manufacturer Celestica and an unnamed Asian ODM for manufacture of CPEs. Yatish named Sequans as their chosen WiMAX chip supplier.

Some additional factors that make deployment in India to reach a broad range of customers, including a large population with low per-capita incomes, are the following:

• The ease of obtaining permits and other rights for construction.

• Low cost of real estate in suburban and rural areas

• Very low cost of installation (truck rolls), $30-$60 US, compared to $150-$300 in America.

• Pent-up demand due to lack of existing phone lines and broadband service.

Yatish said that BSNL has waiting lists of pre-qualified customers that can be converted to WiMAX. WiMAX will provide higher bandwidth than DSL, particularly on the uplink.

• Government support.

• Three times the population of America.

• Very low penetration rate for competitive broadband service.

BSNL has a huge population to sell into but they must have very low pricing for products and service to reach a large segment of the population. They plan to pursue the goal of reaching 20 million people with low cost CPEs and building of thousands of kiosks which can serve hundreds of people each. Developing markets can face similar deployment scenarios: large under-served populations but also demographics, backhaul, power provisioning, and connection to the international Internet backbone must also be taken into account.

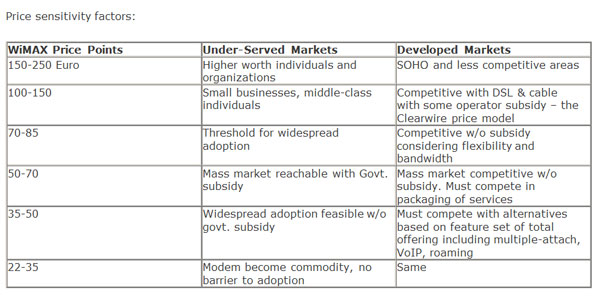

Over the past few years I have asked suppliers including Telsima and others inside India and several international suppliers, government officials, and Indian operators including BSNL about price levels needed to open up various segments of the market demographics. The response is to that the Indian market is highly price-elastic and needs to reach a CPE ASPs of less than $120 to open up a large segment of the population that is characterized by lower incomes. Moving lower in price opens up the market further: it is though that pricing of $100 or less combined with the strategy of spreading availability through kiosks, libraries, schools and other locations will open up a large percentage of the population. Of course, further declines in pricing, higher mobility and greater embedded device availability can aide overall rates of adoption.

BSNL, Wateen, Packet One Networks Deployments Will Drive The WiMAX Price/Volume Tipping Point

While Sprint needs to have CPEs, competitive mobile devices, embedded laptops and UMPCs and aggressive marketing to make their launch a success, BSNL needs only two things to initially to begin the launch to achieve multi-million unit volume: rapid deployment of networks to service waiting customers and low price. Soma’s Yatish said that they do not need to wait for certifications or for availability of additional subscriber units to fulfill initial goals for deployments. Although expressing realistic attitude about potential growth pains, Yatish said, “We just need to execute which we are confident we can do.”

We do not have detailed forecasts for unit volume but believe volume will reach that needed to drive pricing of CPEs down to the target level of about $100/CPE. This has an impact to help Sequans and other suppliers achieve a competitive cost structure for sales that will nudge other markets over the tipping point. Similar to BSNL, several operators around the world have indicated that as lower price levels are achieved they anticipate extending service to broader segments of the population.

Are We There Yet?

The problem with vague market monikers such as ‘tipping points’ is in knowing when they are reached. Pundits often make forecasts that fail to materialize and sometimes fail to see them until months or years after they have occurred. Maravedis surveys the market and build our models for levels of pricing and how that can be expected to change as volumes increase. We monitor trends in planned, actual deployments, and subscriber growth (see www.wimaxcounts.com). We believe we have a fair appraisal of market impacts as key thresholds including ASPs are reached. Therefore, we think the BSNL deployments may be a contributing nudge that sends the WiMAX tipping point over the edge.

By no means is BSNL the only catalyst: like all global communications adoption phenomena, it takes many participants to reach breakthrough levels in pricing and ecosystem development that cascades into success.

WiMAX, WBB deployments must also consider additional factors including power availability, access to international Internet/data backbone networks and providing multiple tiered services and customer owned deployments.

In future articles and in our research reports, we observe unfolding developments in emerging and developed markets that can shift factors for consideration of WiMAX. Certainly, the most price sensitive, high volume deployments will help determine the overall viability and momentum for WiMAX. Deployments will grow increasingly complex as new services evolve and enhanced wireless networking techniques develop.