For decades, the semiconductor supply chain appeared to be one of globalization’s most seamless triumphs. It was an intricate, transcontinental system so efficient that its vulnerabilities went largely unnoticed. That certainty has dissolved. A cascade of shocks, from pandemic-era shortages to escalating tensions between the U.S. and China, has revealed that the world’s most essential technology depends on a supply chain balanced on a geopolitical fault line. What once seemed like an optimized network of specialized production now appears to be a strategic liability. The core infrastructure of the digital age is concentrated in a handful of facilities, on a handful of islands, under intensifying military and economic pressure. The semiconductor industry’s evolution from American dominance to extreme East Asian concentration shows how efficiency gradually eclipsed resilience. Restoring balance has become one of the defining strategic challenges of the 21st century.

To understand how this vulnerability emerged, it is necessary to return to the moment when the trajectory of the global semiconductor industry was first defined. The transistor’s invention at Bell Labs in December 1947 launched an era of American dominance in semiconductor manufacturing.1 For decades, U.S. companies like Intel, Texas Instruments and IBM designed and fabricated chips entirely in-house, controlling every step from conception to production. This vertical integration model thrived through the 1990s, when the U.S. held roughly 40 percent of global semiconductor manufacturing capacity.2

The shift began as Moore’s Law, the observation that transistor density doubles approximately every two years, created relentless pressure to innovate while controlling costs. In 1987, Morris Chang founded Taiwan Semiconductor Manufacturing Company (TSMC), pioneering the foundry model where one company manufactures chips designed by others.3 This innovation sparked the fabless movement in the U.S., where companies invested heavily in chip design while outsourcing manufacturing to Asian contractors. American manufacturing share plummeted from 40 percent in 1990 to around 12 percent by 2020.2 By the 2000s, the industry had fractured into hyper-specialized segments scattered across continents. East Asia accounted for over 80 percent of global chip fabrication capacity by the late 2010s, with Taiwan and South Korea together accounting for 45 percent of global production.4

The production of a single chip involves more than 500 discrete stages and takes between four and six months, with no single country capable of performing all roles in the supply chain independently.5 A finished chip contains components that have traveled over 25,000 miles by the time of final product integration.6 Design software originates primarily from the U.S., while assembly, testing and packaging facilities are concentrated in Taiwan, China and Southeast Asian nations, including Singapore, Malaysia, Vietnam and the Philippines.7 The Netherlands maintains exclusive control over extreme ultraviolet lithography equipment through ASML.8 This complex choreography maximized efficiency and minimized costs but created a system where no single nation could independently produce advanced semiconductors. Through this, efficiency had decisively trumped resilience.

TSMC’s ascent to unprecedented dominance emerged directly from these structural changes. The company’s pure-play foundry model established it as a trusted partner that never competed with its customers, including AMD, Apple, Qualcomm and Nvidia.9 This neutrality created a sustainable competitive advantage as the industry fragmented, allowing TSMC to secure contracts across the entire spectrum of fabless semiconductor firms.

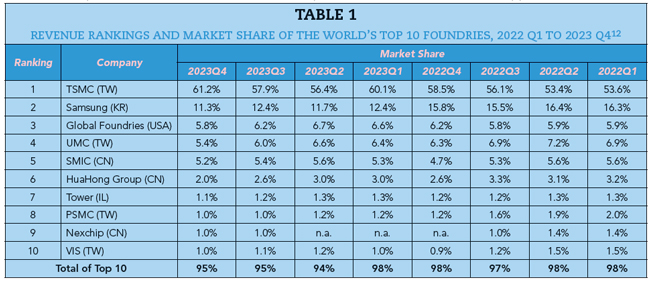

TSMC’s market dominance stems from sustained investment in technology leadership. The company consistently invests 7.1 percent of annual revenue in research and development, spending $6.2 billion in 2024 alone.10 This commitment enabled TSMC to reach advanced process nodes ahead of competitors, becoming the first to mass-produce chips using 7 nm technology in 2018 and to maintain this lead through 5 nm and 3 nm generations.11 By 2023, TSMC controlled approximately 60 percent of the global foundry market, as shown in Table 1, and over 90 percent of the market for chips below 10 nm.12 This technological edge transformed customer preference into customer dependency. Apple contributes 25 percent of TSMC’s revenue, while Nvidia and AMD contribute 11 percent and 7 percent, respectively.13 All three companies have already reserved TSMC’s 3 nm production capacity through 2026.13 When Apple designs iPhone processors, or Nvidia creates AI accelerators for data centers, there is no viable alternative to TSMC for manufacturing at the required performance level. This concentration has created what analysts call a “silicon shield,” the theory that Taiwan’s indispensable role in global chip production deters Chinese military aggression, as any conflict would devastate the world’s digital infrastructure.14 What began as an innovative business model has evolved into a critical vulnerability, with the world’s technology supply concentrated on a single island 90 miles from mainland China.

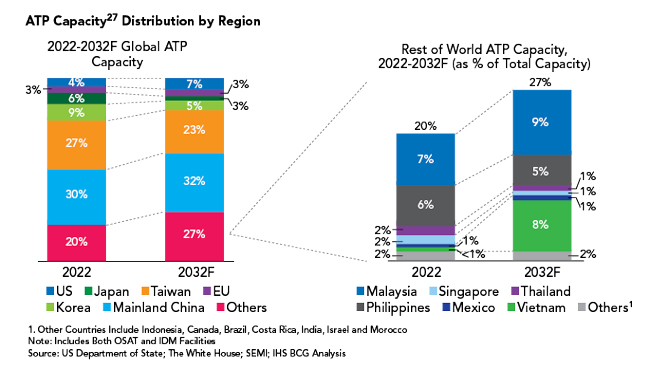

TSMC’s market dominance represents only one choke point in the semiconductor supply chain, as the production process extends well beyond the foundry walls. Chips fabricated in geographically secure locations must still travel to packaging and assembly facilities, with over 95 percent of these concentrated in Taiwan, China and Southeast Asia.5 This concentration has become particularly concerning as packaging has evolved from a simple final step into a critical technological process, yet the U. S. retained virtually no domestic capacity. When the U.S. Department of Commerce prepared arguments for the CHIPS Act, it determined that only 3 percent of packaging occurred in the U.S., with little to no capacity for advanced packaging.15

This geographic concentration, as shown in Figure 1, reflects decisions made when packaging was viewed as low-value commodity work. Southeast Asia represented nearly 20 percent of global assembly, testing and packaging capacity in 2022, which is led by Malaysia at 7 percent and the Philippines at 6 percent. The region’s share is projected to rise to 27 percent by 2032.16 Big companies offshored these labor-intensive operations to regions where wages were a fraction of Western levels. The cost savings appeared to justify the geographic distance.

Figure 1 Assembly, testing, packaging (ATP) capacity distribution by region.16

That tradeoff no longer holds. Packaging technology has undergone a revolution, with advanced techniques like chiplet architectures, 3D stacking and heterogeneous integration now delivering performance improvements comparable to those of transistor scaling. When Nvidia designs its latest AI accelerators, the chips must be packaged using TSMC’s specialized chip-on-wafer-on-substrate (CoWoS) technology, with TSMC’s CoWoS capacity concentrated entirely in Taiwan.17 Nvidia alone has secured 60 percent of total CoWoS capacity through 2026,17 with Apple’s processors similarly dependent on advanced packaging unavailable elsewhere.

The U.S. Department of Commerce acknowledged that “it is cost-prohibitive to bring conventional packaging back to the U.S.,”15 as decades of Southeast Asian dominance have created specialized supplier ecosystems and process knowledge that cannot be rapidly replicated. For decades, policymakers accepted these dependencies as the price of efficiency. Then, between 2018 and 2022, a convergence of geopolitical shocks shattered that consensus.

First came China’s explicit challenge to U.S. technological leadership. In 2015, Beijing launched its “Made in China 2025” initiative with an ambitious goal to increase the Chinese domestic content of core materials to 40 percent by 2020 and 70 percent by 2025, with semiconductors at the center of this reindustrialization plan.18 The Chinese government earmarked an estimated $300 billion to achieve technological self-sufficiency,19 signaling that semiconductors had become instruments of geopolitical competition rather than mere commercial products.

These concerns became acute when the COVID-19 pandemic exposed the fragility Washington had long ignored. Chip shortages forced global automakers to halt production, with estimated losses exceeding $110 billion by May 2021 and more than 9.5 million light-vehicle units lost in 2021 alone.20 The worldwide shortage affected more than 169 industries between 2020 and 2023,21 demonstrating how deeply semiconductor vulnerabilities could disrupt the global economy. What had seemed like an acceptable tradeoff between efficiency and security suddenly seemed reckless.

The final shock came in August 2022. When U.S. House Speaker Nancy Pelosi visited Taiwan, China launched unprecedented military exercises around the island in response to what Beijing viewed as a provocation and implicit endorsement of Taiwanese independence. China fired ballistic missiles over Taiwan and deployed over 100 warplanes and 10 warships in live-fire drills that essentially eliminated the tacit median line separating Chinese and Taiwanese forces.22 Chinese military aircraft made 563 incursions across the median line following Pelosi’s visit, compared to only 23 total crossings in all prior years.23 The exercises underscored how quickly a conflict could cut off access to TSMC’s irreplaceable production capacity. Policymakers confronted an uncomfortable truth: a conflict in the Taiwan Strait would instantly sever the world’s access to advanced semiconductors, disrupting everything from smartphones to weapons systems. Theoretical vulnerability had become an immediate strategic threat. The reclassification of semiconductors from commercial commodities to critical national security technology was complete.

Beginning in 2022, the U.S. launched the most significant semiconductor industrial policy intervention since the Cold War, driven by this transformed understanding of strategic vulnerability. The U.S. adopted a comprehensive approach centered on incentives for large-scale manufacturing, stringent export controls to limit China’s access to advanced technologies and closer coordination with allied partners. Together, these measures marked a decisive break from decades of market-driven development and redefined the strategic landscape of global semiconductor policy.

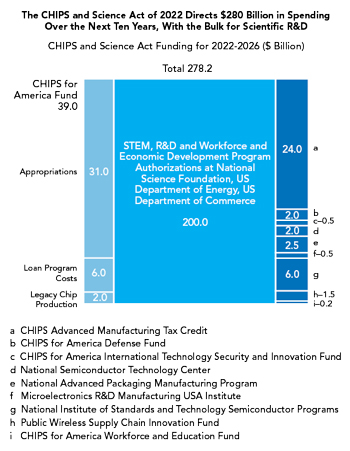

Figure 2 CHIPS and Science Act funding for 2022 to 2026, $ billion.24

The CHIPS and Science Act, signed into law on August 9, 2022, represents a $280 billion investment over 10 years to rebuild America’s semiconductor manufacturing base and advance scientific innovation.24 Of this total, $200 billion is dedicated to broader scientific research and development and commercialization efforts in emerging technologies,24 as shown in Figure 2. The semiconductor-specific allocation of $52.7 billion breaks down into $39 billion for manufacturing incentives, $11 billion for research and development programs and $2 billion for defense-related chip production.24 Additionally, the legislation provides $24 billion in tax credits to further stimulate domestic chip production.24 These subsidies aimed to overcome a fundamental economic reality: producing advanced chips in the U.S. costs substantially more than in Asia due to higher labor costs, less developed supply chains and the absence of the specialized supplier ecosystems that had emerged over decades in East Asia.

The Commerce Department structured awards to encourage not just fabrication facilities but the entire ecosystem, including materials suppliers, equipment manufacturers and packaging operations. Significant commitments quickly followed. TSMC announced a $40 billion investment to build two fabs in Arizona.25 Intel pledged over $100 billion for facilities in Ohio and Arizona.26 Samsung committed $17 billion to a fabrication plant in Texas.27 These projects represented attempts to rebuild capabilities that had been offshored over three decades, with subsidies designed to make economically irrational domestic production financially viable.

Financial incentives alone could not address the immediate security concern of China’s technological advancement. In October 2022, the Bureau of Industry and Security imposed sweeping export controls on advanced computing chips, semiconductor manufacturing equipment and related technology destined for China.28 These restrictions went beyond traditional sanctions. They prohibited the sale of any advanced chip manufactured anywhere in the world using American technology to Chinese AI companies or military end users.28 This approach leveraged a crucial asymmetry in which virtually all global chipmakers depend on U.S. software, equipment or intellectual property. It gave the U.S. extraterritorial reach, effectively controlling semiconductor trade well beyond its borders. The regulations blocked China’s access to extreme ultraviolet lithography systems, essential technology for producing chips at advanced nodes, and prohibited U.S. citizens from supporting chip development at certain Chinese fabrication facilities.29

Recognizing complete self-sufficiency was neither feasible nor desirable, the third element focused on alliance coordination. The Chip 4 framework brought together the U.S., Japan, South Korea and Taiwan, the four economies controlling most of the advanced semiconductor production and technology.30 Japan contributed its strengths in materials and equipment manufacturing, particularly Tokyo Electron’s lithography and etching tools.30 South Korea brought Samsung and SK Hynix’s dominance in memory chips and advanced logic capabilities.31 Taiwan provided TSMC’s leading-edge foundry production.31 The framework established mechanisms for coordinating export controls, sharing supply chain data and jointly funding research into next-generation technologies. In parallel, the U.S. worked to align European policy through the EU Chips Act, which committed €43 billion to semiconductor development.32 Rather than replicating the entire supply chain domestically, this approach acknowledged continued interdependence with trusted partners while collectively restricting China’s access to critical technologies. The strategy prioritized resilience through alliances over total self-reliance, attempting to create a “small yard, high fence” that protected the most sensitive technologies while maintaining commercial relationships in less critical areas.

These policies appeared comprehensive on paper. In practice, translating legislation into operational fabs and reshored supply chains proved more complex than anticipated. Three years into the CHIPS Act era, the U.S. has secured commitments for over $200 billion in semiconductor investment across more than 40 new projects,33 yet operational capacity remains years away and critical gaps persist. The disparity between announced funding and the production lines in operation has become increasingly apparent. Major fabrication projects are underway at facilities announced by TSMC, Samsung and Intel, but none have yet reached high-volume production. TSMC’s first Arizona fab began mass production in the fourth quarter of 2024, while its second fab was pushed back to 2027 or 2028,34 illustrating how timelines from groundbreaking to operational production have stretched far beyond initial projections.

Persistent dependencies undermine aspirations for supply chain independence. The U.S. relies entirely on ASML in the Netherlands for extreme ultraviolet lithography machines. The Dutch company maintains a monopoly as the sole supplier of EUV systems, which are essential for manufacturing chips at 7 nanometers and below.35 No American alternatives exist, nor are any under development. Meanwhile, domestic packaging and assembly infrastructure remains nascent, with most advanced packaging still concentrated in Asia. Economic realities compound these challenges, as manufacturing chips in the U.S. costs 30 to 50 percent more than in Asia due to higher labor, energy and regulatory costs.36 CHIPS Act subsidies help narrow this gap, but cannot eliminate the fundamental cost disadvantages that drove offshoring in the first place.

TSMC’s Arizona facility illustrates these obstacles. Announced with great attention and $40 billion in committed investment, the project faced repeated delays. Production originally scheduled for late 2024 was pushed to 2025 due to insufficient skilled workers for specialized equipment installation.37 CEO Che-Chia Wei attributed delays to complex compliance requirements and extensive permitting processes, with approval timelines taking at least twice as long as in Taiwan.38 The company deployed approximately 500 Taiwanese personnel to Arizona and sent 600 American engineers to Taiwan for over a year of training, during which they struggled with language barriers, 12-hour workdays and a hierarchical management culture.39 Replicating Taiwan’s supplier ecosystem, built over decades, proved far harder than writing checks, underscoring that transplanting semiconductor manufacturing requires more than financial capital alone.

The effort to rebuild semiconductor resilience confronts a paradox: the very forces that created vulnerability make it nearly impossible to eliminate. Three years of policy intervention have demonstrated that subsidies can attract investment announcements, but cannot rapidly conjure the supplier ecosystems, technical expertise and cost structures that took East Asia decades to develop. While new incentives are expanding domestic fabrication, the gains remain modest and fail to alter structural supply chain dependencies. ASML’s monopoly on EUV lithography persists. Advanced packaging remains concentrated in Taiwan and Southeast Asia. The skilled workforce required to operate fabs cannot be trained overnight.

Given these constraints, complete supply chain independence remains unattainable, and efforts to achieve it may only result in expensive facilities that lack commercial viability. A more attainable strategy involves fostering managed interdependence across a network of aligned nations. The Chip 4 framework represents this pragmatic approach, distributing critical capabilities across trusted partners rather than replicating everything domestically. Japan provides materials and equipment, South Korea contributes memory production, Taiwan maintains leading-edge logic fabrication, and the U.S. focuses on design and selected manufacturing. Such an arrangement balances economic efficiency with reduced dependence on single points of failure.

Nevertheless, this more restrained vision still encounters significant obstacles. Effective coordination among allies demands the alignment of often competing economic interests and security objectives. Export controls that protect American technological advantages may disadvantage South Korean and Taiwanese firms competing in global markets, while subsidy competitions among allies risk zero-sum outcomes when governments bid against one another for the same facilities. Without resolution of the underlying cost differentials that prompted offshoring, domestic semiconductor manufacturing will require continuous government intervention to remain viable. Achieving meaningful supply chain resilience will require long-term commitment across four areas: technical infrastructure, economic incentives, workforce development and coordination with allies. It is a decade-long effort that will require sustained political commitment across multiple administrations.

The semiconductor industry’s transformation from globalization’s triumph to its most glaring vulnerability reveals how optimization for efficiency can create catastrophic strategic exposure. What began with the transistor’s invention at Bell Labs evolved over decades of specialization into a system in which the world’s most critical technology depends on facilities concentrated in a geopolitically contested region. The pandemic, China’s technological ambitions and military tensions around Taiwan shattered the illusion that such dependencies were sustainable. The policy response, centered on the CHIPS Act and export controls, represents a fundamental break from market-driven development. Nevertheless, the path forward is marked by uncertainty. Reshoring advanced manufacturing proves far more difficult than anticipated, costs remain prohibitive without permanent subsidies and true independence remains impossible. The question is no longer whether the semiconductor supply chain will remain vulnerable, but whether managed interdependence among allies can provide enough resilience to navigate the geopolitical pressures of the coming decades.

References

- R.U. Ayres, “The transistor transition: 1945–1969,” The History and Future of Technology: Can Technology Save Humanity from Extinction?, Cham: Springer International Publishing, 2021, pp. 425–466.

- G. Arcuri and S. Lu, “Taiwan’s Semiconductor Dominance: Implications for Cross-Strait Relations and the Prospect of Forceful Unification| Perspectives on Innovation| CSIS,” Center for Strategic and International Studies (CSIS), March, 22, 2022.

- K. Montevirgen, “Taiwan Semiconductor Manufacturing Co. (TSMC),” Encyclopedia Britannica, 2025, Web: https://www.britannica.com/money/Taiwan-Semiconductor-Manufacturing-Co.

- H.W.C. Yeung, “Explaining geographic shifts of chip making toward East Asia and market dynamics in semiconductor global production networks,” Economic Geography, 98(3), 2022, pp.272–298.

- A. Thadani and G.C. Allen, “Mapping the Semiconductor Supply Chain,” Center for Strategic and International Studies, May, 11, 2023.

- D. Lotta, “Project 2049 Institute & US-Taiwan Business Council 2023,” United States, Taiwan, and Semiconductors: A Critical Supply Chain Partnership – Final Report, Project 2049 Institute & US-Taiwan Business Council, June 21, 2023, Web: https://www.us-taiwan.org/wp-content/uploads/2023/06/2023.06.21-Final-Semiconductor-Report.pdf.

- R. Rasiah, X.S. Yap and S.F. Yap, “Sticky spots on slippery slopes: The development of the integrated circuits industry in emerging East Asia,” Institutions and Economies, pp.52–79, 2015.

- J. VerWey, “Tracing the Emergence of Extreme Ultraviolet Lithography,” Center for Security and Emerging Technology, July 2024.

- M. Lee, M.H Weng and S.L. Jang, “The Competitiveness and Future Challenge of the Taiwan Semiconductors Industry. In Technology Rivalry Between the USA and China,” Cham: Springer Nature Switzerland. 2025, pp. 161–206.

- “Taiwan Semiconductor Manufacturing Company, 2024,” TSMC Business Overview 2024, Web: investor.tsmc.com/sites/ir/annual-report/2024/2024%20Business%20Overview_0.pdf.

- M. Spencer, “TSMC’s role in global AI and geopolitical order - a Full Report,” AI Supremacy, 2025, Web: https://www.ai-supremacy.com/p/tsmc-role-in-the-global-ai-and-geopolitical-future

- C. Y. Tung, “Taiwan and the global semiconductor supply chain: 2023 in review,” Representative Taipei Representative Office in Singapore, 2024.

- PredictStreet, “TSMC: The Unseen Giant Powering the Future of technology,” The Chronicle-Journal, 2025, Web: https://markets.chroniclejournal.com/chroniclejournal/article/predictstreet-2025-9-30-tsmc-the-unseen-giant-powering-the-future-of-technology.

- D.P. Chen, “US Industrial Policy for the Twenty-First Century: The Washington-Taipei Techno-Democracy Partnership Amidst Chip Rivalry with Beijing,” Technology Rivalry Between the USA and China, Cham: Springer Nature Switzerland, 2025, pp. 27–57.

- “Frequently Asked Questions: CHIPS Act of 2022 Provisions and Implementation, Congress.gov, Web: https://www.congress.gov/crs-product/R47523.

- R. Varadarajan, I. Koch-Weser, C.H. Richard, J.O. Fitzgerald, J.A. Singh, M.A. Thornton, R.O. Casanova and D.A. Isaacs, “Emerging resilience in the semiconductor supply chain,” Boston Consulting Group and Semiconductor Industry Association, 2024.

- R. Noor, H.R. Kottur, P.J. Craig, L.K.Biswas, M.S.M. Khan, N. Varshney, H. Dalir, E. Akçalı, B.G. Motlagh, C. Woychik and Y.K. Yoon, “US microelectronics packaging ecosystem: Challenges and opportunities,“ arXiv preprint arXiv:2310.11651, 2023.

- A. Janjeva, S. Baek and A. Sellars, “ China’s Quest for Semiconductor Self-Sufficiency,” 2024.

- M.J. Zenglein, and A. Holzmann, “Evolving made in China 2025,” MERICS papers on China, 8, 2019, p.78.

- V. Ramani,D. Ghosh and M.S. Sodhi, “Understanding systemic disruption from the Covid-19-induced semiconductor shortage for the auto industry,” Omega, 113, 2022, p.102720.

- D. Howley, “These 169 industries are being hit by the global chip shortage,” Yahoo Finance, 2021.

- T. Shattuck, “One Year Later: How Has China’s Military Pressure on Taiwan Changed Since Nancy Pelosi’s Visit?,” Global Taiwan Brief, 8(18), 2023, pp.9–11.

- R. Hsiao, “Taiwan and South Korea Enhancing Their Engagement as Chinese Aggression Intensifies. Global Taiwan Institute, Global Taiwan Brief, 8, 2023.

- J. Badlam, S. Clark, S. Gajendragadkar, A. Kumar, S. O’Rourke and D. Swartz, “The CHIPS and Science Act: What is it and what is in it?,” McKinsey & Company, 2022, Web: https://www.mckinsey.com/industries/public-sector/our-insights/the-chips-and-science-act-heres-whats-in-it.

- “TSMC Announces Updates for TSMC Arizona,” Taiwan Semiconductor Manufacturing Company Limited, 2022, Web: https://pr.tsmc.com/english/news/2977.

- “Intel, Biden-Harris Administration Finalize $7.86 Billion Funding Award Under US CHIPS Act,” Intel Newsroom, 2024, Web: https://newsroom.intel.com/corporate/intel-chips-act.

- “Samsung Electronics Announces New Advanced Semiconductor Fab Site in Taylor, Texas,” Samsung News, 2021, Web: https://semiconductor.samsung.com/sas/local-news/samsung-electronics-announces-new-advanced-semiconductor-fab-site-in-taylor-texas/.

- “CHIPS, China and Choke Points: The Economic and National Security Consequences of US Semiconductor Export Control Policy,”NYUJ Int’l L. & Pol., 57, 2024, p.456.

- J. Edwards, “Chips, subsidies and commercial competition between the United States and China,” Regaining Growth Momentum after the Pandemic, 2024, p.213.

- M.A. Peters, “Semiconductors, geopolitics and technological rivalry: the US CHIPS & Science Act,” 2022. Educational Philosophy and Theory, 55(14), 2023, pp.1642–1646.

- F. Jia, D. Hu, T. Zhang, L. Chen and M.L. Tseng, “Global semiconductor supply chain: a national competitiveness analysis,” International Journal of Production Research, 2025, pp.1–20.

- J.V. Camps and A. Saz-Carranza, “The European Chips Act: Europe’s Quest for Semiconductor Autonomy,” Center for Global Economy and Geopolitics, 2023, pp.10–17.

- P. Gerhard and T.W. John, “Joseph R. Biden, Jr., ICYMI: The CHIPS Act Has Already Sparked $200 Billion in Private Investments for U.S. Semiconductor Production,” The American Presidency Project, 2021, Web: https://www.presidency.ucsb.edu/node/359102.

- “TSMC Arizona’s Rocky Road: Delays, Soaring Costs, and the Future of Global Chip Manufacturing, Wral News, 2025, Web: https://markets.financialcontent.com/wral/article/tokenring-2025-10-2-tsmc-arizonas-rocky-road-delays-soaring-costs-and-the-future-of-global-chip-manufacturing.

- T.V.A. Quach, “A Chips industry in Europe: feasibility and viability in a global context,” 2025.

- A. Varas, R. Varadarajan, J. Goodrich and F. Yinug, “Turning the Tide for semiconductor manufacturing in the U.S.,” SIA/BCG Report Government Incentives and U.S. Competitiveness in Semiconductor Manufacturing, 2020, Web: https://www.semiconductors.org/turning-the-tide-for-semiconductor-manufacturing-in-the-u-s/.

- N. Gordon, “TSMC claims it can’t find enough skilled workers to get its Arizona chip plants ready in time, delaying mass production to 2025,” Fortune, 2023, Web: https://fortune.com/2023/07/21/tsmc-complains-cant-find-enough-skilled-workers-arizona-chip-plants-ready-delay-mass-production-2025/.

- P.A. Thomas, “Delays in TSMC’s Arizona plant spark supply chain worries,” CIO, 2025, Web: https://www.cio.com/article/3806430/delays-in-tsmcs-arizona-plant-spark-supply-chain-worries.html.

- V. Zhou, “TSMC’s Debacle in the American Desert,” Rest of World, 2024, Web: https://restofworld.org/2024/tsmc-arizona-expansion/.