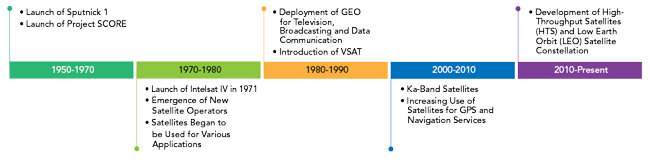

A new era of space exploration and innovation opens transformative possibilities for governments and companies in the satellite communications (satcom) sector. Satcom services provide vital global connectivity by transmitting data, voice and video signals via satellites. This ensures access to communication networks in remote and underserved areas lacking terrestrial infrastructure. These services are essential across various sectors, including broadcasting, military, maritime and enterprise, offering reliable high speed connections that support real-time data transfer, high-definition content distribution and critical communications during emergencies and disasters. As demand for seamless connectivity grows, driven by the expansion of IoT, the need for broadband internet in rural regions and the increasing reliance on digital services, satcom continues to evolve with advancements such as high-throughput satellites (HTS) and low Earth orbit (LEO) constellations. These innovations are enhancing capacity, speed and coverage, making satcom an indispensable component of the global communications infrastructure, particularly in regions where other forms of connectivity are not feasible. According to MarketsandMarkets, the satcom market is estimated to reach $33.2 billion by 2029 at a compound annual growth rate (CAGR) of 14.5 percent.1 Figure 1 shows a brief history of some of the most critical developments in the evolution of the satcom market.

Figure 1 The evolution of the satellite communications market. Source: Secondary research, interviews with experts and MarketsandMarkets analysis.

In the short term, the satcom market is expected to witness steady growth driven by increased demand for connectivity in remote and underserved areas. Providers will focus on enhancing service quality and expanding coverage to meet rising maritime, aviation and emergency service needs. Technological advancements will be centered around improving data transmission speeds and network reliability. Innovations will likely involve better integration of satellite services with existing terrestrial networks to enhance overall performance and service delivery.

MID-TERM ROADMAP (2026 TO 2028)

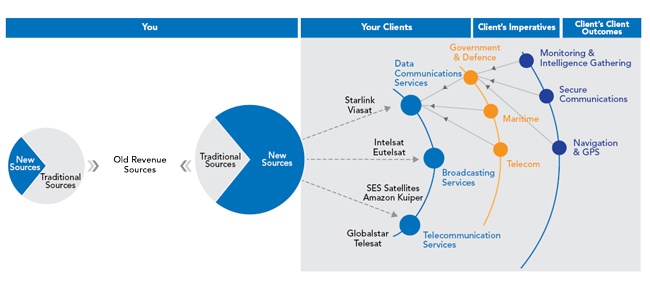

The mid-term period will witness a significant evolution in satcom services, with a greater emphasis on leveraging emerging technologies. The integration of services with advanced technologies, such as IoT and 5G, will be a key trend, enabling more seamless and efficient communication. Providers will focus on enhancing service customization and adaptability to meet diverse user needs and applications. Technological advancements will include improved signal processing and dynamic bandwidth management, contributing to more robust and flexible service offerings. Figure 2 shows MarketsandMarkets’ thoughts on some of the satcom market participants, segments and applications, with typical interconnections shown for Starlink and Viasat.

Figure 2 Satellite communications market. Source: Secondary research, interviews with experts and MarketsandMarkets analysis.

LONG-TERM ROADMAP (2029 and BEYOND)

Looking ahead, the satcom market is set for exciting changes driven by advancing technologies. As satellite services merge with next-generation innovations, new applications and use cases will emerge that can reshape connectivity. Services will become more flexible, offering tailored solutions that integrate seamlessly with smart infrastructure and real-time data insights. The focus will shift toward making everything run more smoothly and efficiently, thanks to AI-driven management and automation improvements. This evolution will solidify satcom services as a fundamental component of global connectivity in a more interconnected world.

Ground stations are the essential hubs of communication between satellites and the Earth. They consist of large antennas, often called parabolic dishes, responsible for transmitting and receiving data to and from orbiting satellites. These stations are complex facilities equipped with tracking systems to maintain alignment with the fast-moving satellites. Modern ground stations incorporate technologies like adaptive coding and modulation, which adjust signal quality in response to changing atmospheric conditions to ensure data reliability. With advances in automation, many ground stations can now operate with minimal human intervention, continuously communicating with satellites across various orbits from LEO to geostationary orbit (GEO). Essentially, ground stations are the terrestrial link in the satcom chain, managing massive amounts of data and ensuring it reaches its intended destination efficiently.

FREQUENCY BANDS

Frequency bands play a crucial role in satcom services. Each of the satellite bands has unique properties that affect data transmission between satellites and ground stations. The L-Band, from 1 to 2 GHz, is valued for its ability to penetrate weather conditions like rain and fog, ensuring reliable communication in adverse weather. The disadvantage of L-Band is lower data transfer rates. The S-Band, between 2 and 4 GHz, offers a balance between coverage and data rate. This band is suitable for satellite and mobile applications requiring better performance than L-Band can provide but with less capacity. The C-Band, ranging from 4 to 8 GHz, is commonly used for satellite TV and communication, providing stable coverage and data rates with less susceptibility to rain fade than higher frequencies. The X-Band, from 8 to 12 GHz, is mainly used for military and government communications, offering higher data rates and precision. However, this band is affected by rain and atmospheric interference more than lower frequency bands. The Ku-Band, covering 12 to 18 GHz, supports high data rate communications, making this band ideal for broadband and satellite TV. However, this band is more prone to rain fade effects. The Ka-Band, from 18 to 40 GHz, is used for high-capacity applications like high speed internet. This band enables very high data rates and bandwidth but is significantly impacted by atmospheric conditions such as rain and humidity. Dynamic spectrum management is essential in today’s satcom environment to optimize these bands, reduce data congestion and ensure that diverse applications, from TV broadcasts to internet services, function efficiently without interference.

TERRESTRIAL NETWORKS

Terrestrial networks are integral to satcom services, acting as the essential infrastructure that connects satellite signals to end users and integrates them with broader communications systems. These networks encompass a range of technologies, including fiber optics, microwave links and other high-capacity transmission mediums that ensure efficient data flow from satellite ground stations to various endpoints. Fiber-optic cables provide high speed, high bandwidth connections crucial for handling the large volumes of data transmitted from satellites. In areas where fiber deployment is not feasible, microwave links are the preferred technology for point-to-point connections. Additionally, terrestrial networks incorporate advanced networking technologies like software-defined networking and network function virtualization, enhancing flexibility and efficiency by allowing dynamic management and optimizing data traffic. This integration ensures that satellite-delivered data can be effectively distributed to homes, businesses and mobile devices, supporting a seamless and reliable communications experience across diverse applications and geographical locations.

MARKET FORECASTS

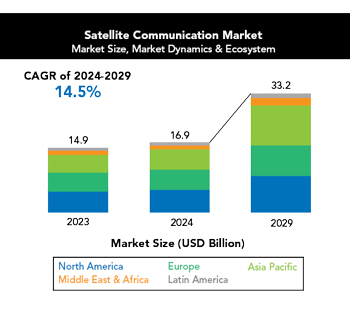

Figure 3 Satellite communications market forecast. Source: Secondary research, interviews with experts and MarketsandMarkets analysis.

The satcom market is expected to reach $33.2 billion by 2029 from $16.9 billion in 2024, at a CAGR of 14.5 percent from 2024 to 2029. The Asia-Pacific segment of the satcom market will be the largest in 2029, followed by North America and Europe. Africa and the Middle East are constantly in flux due to different developments and strategic initiatives. However, while remaining small, these regions will present opportunities for higher growth rates in the next five years. The expected increase in the market, along with regional segmentation, is shown in Figure 3.

CONCLUSION

Whether consumers or businesses, users are showing an insatiable desire for connectivity and data-intensive services. As the demand grows for seamless connectivity, satcom networks are playing a vital role in evolving data, voice and video networks. The drivers for the evolution of satellite networks’ role in connectivity include increased demand from remote, underserved areas, an expansion of IoT and M2M communications, increasing service demand from maritime, aviation, broadcasting and security applications and partnerships with 5G operators.

While the opportunity is significant and the drivers are strong, challenges still remain. The industry is characterized by high initial investment and operational costs. Like terrestrial wireless networks, there are regulatory and spectrum allocation challenges and the satellite networks must develop an approach that allows them to coexist with terrestrial networks. From a technology standpoint, latency performance and bandwidth availability will not be sufficient for some applications. Paradoxically, the success of the satellite network may pose the most significant challenge. As more satellites are launched into larger and denser constellations, space debris and satellite failures pose an increasing risk to all satellites. However, MarketsandMarkets’ forecast shows revenue in the satellite market nearly doubling in five years, the industry will see success in solving these challenges and capitalizing on the benefits and advantages that satcom networks will provide users.

References

- “Satellite Communication Market by Type, Application and Region - Global Forecast to 2029,” MarketsandMarkets, August 2024, Web: marketsandmarkets.com/Market-Reports/satellite-communication-market-32381348.html.