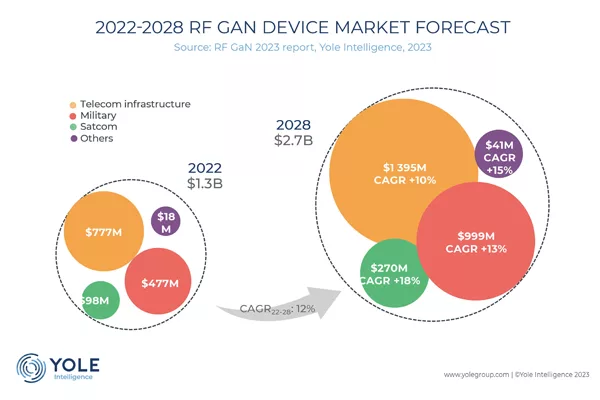

In telecom infrastructure, GaN has penetrated various base stations with its high-power and high frequency performance benefits. With the transition from RRH to AAS in macro/microcells, massive MIMO (mMIMO) requires more power amplifier units per base station. The higher PAE and broadband capability at frequencies above 3 GHz compared to LDMOS is an opportunity for GaN to grow. The GaN-based telecom infrastructure device market will represent almost 45 percent of the total market by 2028.

As a traditional GaN market, the defense segment is one of the main drivers for GaN RF. GaN-on-SiC is still the primary platform supplying demanding applications in defense radar, electronic warfare and defense communication applications.

In this dynamic context, Yole Intelligence releases its annual RF GaN report. This study provides an overview of the market and the players in the various segments, along with their product ranges and technologies. The company, part of Yole Group, outlines each segment’s market dynamics and main technologies. Analysts also explain the requirements of the various RF markets and their corresponding impact on the need for different technologies, along with geographical specificities.

Aymen Ghorbel, technology and market analyst specializing in compound semiconductor and emerging materials at Yole Intelligence said, “As of 2023, GaN-on-SiC is still the primary platform for RF GaN, as the supply chain has been well developed. However, IDM is the preferred business model, as IDMs can benefit from their existing customer channels in the telecom and defense markets.”

In 2022, SEDI, Qorvo and Wolfspeed were the leading players in the RF GaN device business, while NXP has gained significant growth by entering the telecom market’s supply chain. The S.I. SiC wafer market remains shared by the three major suppliers, Wolfspeed, Coherent and SICC. In the defense segment, Raytheon, Northrop Grumman and Chinese CETC are leading GaN adoption. Department of Defense-trusted Wolfspeed and Qorvo are also GaN foundries. Focusing on the suppliers to the telecom market, Ericsson and Nokia continue developing the supply of RF GaN devices to source from multiple suppliers while Samsung cooperates closely with Korean device players. Since the US sanction, Huawei and ZTE have turned to the Chinese supply chain to develop domestic capability.

Poshun Chiu, senior technology and market analyst specializing in compound semiconductors and emerging substrates at Yole Intelligence, part of Yole Group, said, “As of 2023, the mainstream GaN technology is on SiC substrate. The technology has matured and demonstrated good performance at high power and frequency. Over the last years, players like STMicroelectronics with MACOM, Ommic, Infineon and foundries like GlobalFoundries and UMC have been working on introducing RF GaN-on-Si technology. As the telecom small cell requires PAs with lower power, GaN-on-Si can find a sweet spot in 32T32R and 64T64R mMIMO base stations below 10 W. We expect to see GaN-on-Si enter the market starting at the end of 2023 and taking market share in the coming years.”

With technology node evolution, device players developing platforms for the Ku/K/Ka-Bands are even targeting nodes under 0.1 µm for sub-THz frequencies and a potential 6G market in the future. The target of the emerging GaN-on-Si platform for RF applications is a sub-6 GHz small cell by leveraging the efficiency and wide bandwidth at a lower power level. However, considering the complexity of changing the design of handset systems, it’s a longer-term target market for GaN-on-Si.