Cable operators have historically taken a measured approach to improving their broadband networks by adding capacity incrementally through spectrum and modulation improvements. It is an approach that has served them incredibly well over the years, especially when it comes to balancing capital expenditures with the need to be market leaders when it comes to delivering the billboard speeds most subscribers care about. It is also a strategy they have been able to implement in the North American market because of their dominant share of broadband subscribers and homes passed.

However, this dominance is currently facing challenges on two fronts. At the low end of the market, the emergence of 5G fixed wireless services by industry players like T-Mobile, Verizon and AT&T is creating pressure. At the high end, fiber internet service providers (ISPs) expanding their own footprint while also overbuilding their DSL networks with an eye towards eventually decommissioning this aging copper infrastructure provides the challenge.

The net result is that cable operators, who have always had many tools at their disposal to expand broadband throughput and capacity, are accelerating their efforts to, at a minimum, keep pace with burgeoning fiber competition. These efforts involve tried and true methods of cost-effectively upgrading their hybrid fiber coax (HFC) networks through a combination of band splits and distributed access architectures (DAAs). These methods are complemented by greenfield fiber buildouts to new residential developments and via edge-out projects intended to deliver service to unserved and underserved markets.

For a large number of multi-system operators (MSOs) around the world, 2020 and 2021 were the years of node splitting, whereby service group sizes were reduced and available bandwidth increased by either logically or physically segmenting existing HFC optical nodes. These efforts were quick and cost-effective methods to relieve congestion that arose rapidly when the pandemic forced the closure of schools and businesses, pushing utilization rates per node beyond the 70 percent threshold that most MSOs set for themselves.

Those efforts, which are always ongoing, have been complemented by band splits, in the form of either mid-split or high-split upgrades, which pushed upstream bandwidth from 5 to 42 MHz up to 85 to 200 MHz. These efforts, throughout 2022 and continuing today, enable MSOs to push upstream bandwidth from an average of 35 to 50 Mbps to 100 to 200 Mbps. This becomes a better complement to the 1 to 2 Gbps downstream services they were already offering.

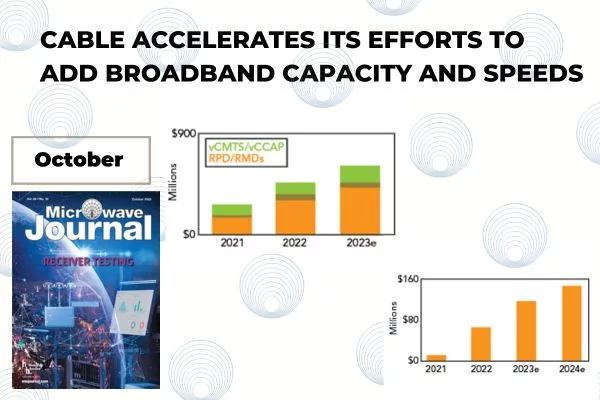

Figure 1 Worldwide DOCSIS equipment revenue. Source: Dell’Oro Group.

The band-splitting work has frequently been done in conjunction with deployments of remote PHY devices (RPDs) and virtual CMTS (vCMTS) platforms. These are viewed as foundational steps toward either the full-duplex (FDD) or extended spectrum (ESD) versions of DOCSIS 4.0. Certainly, those operators moving forward with high-split projects will almost always do so using either RPDs or remote MACPHY devices (RMDs), both of which improve signal quality by taking advantage of digital optics in both the forward and return paths. Dell’Oro’s latest thoughts on the actual DOCSIS equipment revenue for 2021 and 2022, along with the estimate for 2023 are shown in Figure 1.

DOCSIS 3.1 EXTENDED

The transition to DOCSIS 4.0 (D4.0) will be gradual, owing to the significant upgrades that need to be made to the outside plant to enable the speeds offered by both D4.0 variants. FDD D4.0 will require brand-new amplifiers, nodes and modems with DSP silicon that can handle echo cancellation. The integration of echo cancellation into those units will result in additional costs per unit, as well as added complexity. On the positive side, most current taps can remain in place.

The same cannot be said for 1.8 GHz ESD upgrades, which will also require amplifier swaps along with taps and other passive elements. With ongoing labor shortages and costs still a critical consideration of any new buildout, not needing to touch any taps in neighborhoods is very attractive. Furthermore, replacing taps does require temporary service shutdown and this is always an important consideration for operators, especially when their competitors would likely exploit any service disruptions.

ESD, on the other hand, is what operators know. They have decades of experience adding spectrum and capacity through amplifiers, taps and passive swaps. There is no new spacing of the amplifiers to be done. Also, operators can go ahead and upgrade the amplifiers first and then tackle tap upgrades, as most taps in the field today support up to 1.2 GHz. That way, operators can derive some spectrum upgrades without having to do the heavy lifting of tap upgrades right away.

No matter the road operators choose to adopt D4.0, there is no question that there are a lot of moving parts. Taking into account existing supply chain problems and labor shortages, achieving the overall homes passed goals will vary significantly. Though nearly all operators committed to D4.0 concur that all systems are in agreement, it would be very unlike cable operators to have a contingency plan.

That contingency plan involves the deployment of D4.0 modems tied to DOCSIS 3.1 (D3.1) CMTS and vCMTS platforms in high-split configurations. Recent interoperability tests conducted at CableLabs demonstrated downstream speeds of over 8 Gbps and upstream speeds of 1.5 Gbps. This architecture has been dubbed D3.1 Extended (D3.1 E) and it has the attention of operators around the world, particularly those in Europe who have already said they are unlikely to deploy D4.0.

Way back in 2013, when the first D3.1 specifications were released, one of the goals was to deliver 10 Gbps of downstream speeds. Operators and equipment manufacturers envisioned doing this by using a combination of orthogonal frequency division multiplexing (OFDM) channels and modulation orders ranging from 4096-QAM up to 8192-QAM and 16384-QAM over channel bandwidths ranging from 24 to 192 MHz. At the time, operators were universally offering far less than 1 Gbps of downstream speeds, so many of the CMTS platforms and modems only took advantage of the lower end of the standard’s capability.

Today, with 1 Gbps speeds essentially table stakes for operators, MSOs and their vendor partners are working to take advantage of the available capacity through the combination of existing D3.1 CMTS and vCMTS platforms and D4.0 modems, which can support four OFDM channels’ worth of bandwidth. The D4.0 modems, though expensive early on, are an essential purchase that will deliver multi-gigabit speeds even before the outside plant upgrades are complete. Plus, when the infrastructure upgrades are complete, subscribers will already have the modems in place to take full advantage of end-to-end D4.0 capabilities.

D4.0 TO FIBER

Figure 2 Worldwide cable R-OLT revenue. Source: Dell’Oro Group.

While these DOCSIS-based architectures will serve as the backbone for the majority of their residential networks, it is clear that MSOs are aiming to provide more fiber to the home (FTTH) services than previously expected. By relying on a combination of remote PHY and vCMTS to re-architect existing DOCSIS networks and move to DAA, the MSOs can selectively deploy remote optical line terminal (R-OLT) modules alongside RPDs in existing node locations to peel off FTTH service groups of 32 to 64 homes. Traffic originating from those RPD and R-OLT modules can be transported back to the headend via Ethernet transport, with all subscriber endpoints, be they DOCSIS modems or passive optical network optical access point to terminals managed through the same vCMTS and/or virtualized broadband network gateway (vBNG) platforms. Dell’Oro’s latest thoughts on the actual cable R-OLT revenue for 2021 and 2022, along with estimates for 2023 and 2024 are shown in Figure 2.

Another option for MSOs with this architecture is the mixed use of optical nodes for DOCSIS-based residential services and fiber-based business services using the R-OLT. There are many instances of optical nodes covering service groups that include both residential and business customers. Historically, MSOs have only been able to offer business-class DOCSIS services to these customers, with an upcharge for higher service level agreements (SLAs), static IP addresses and other features. MSOs have done extremely well over the last decade in stealing away small- and medium-business customers from telcos who had more inflexible pricing plans or relied on T1 or business-class DSL lines. But recently, telcos and other fiber ISPs have pushed hard to get these business customers back by pitching the higher reliability and technological advantage of fiber. Thus, the availability of R-OLTs, particularly those that can be added into existing node housings without significant upgrades, allows cable operators to offer a comparable fiber service to valuable business customers while evolving their access networks.

Other cable operators are bypassing this evolutionary progression and overbuilding with fiber today. Many of these operators either do not pass millions of homes or are located in countries where the cost to change the outside plant, due to labor, permitting or both, is simply too high for a step-by-step progression. Nevertheless, a clear roadmap for the transition from DOCSIS to fiber now exists and is being operationalized at a growing number of MSOs around the world.