Three years after 5G was officially commercialized, while most of the deployments are primarily focused on 5G mid-band, the development of 5G mmWave technology has also been underway. 5G mmWave, operating in high frequency bands between 24 to 100 GHz, offers faster data transfer rates, low latency and higher bandwidth compared to the previous wireless technology.

However, the deployment of 5G mmWave technology poses challenges beyond its physical characteristics, such as shorter range and susceptibility to interference. One significant challenge is the lack of compelling business use cases that justify its cost and deployment challenges. While the technology offers faster data transfer rates and low latency, the benefits may not be enough to justify the significant investment required to deploy it. Therefore, careful thought is required to identify and prioritize the use cases to provide the most significant impact and return on investment.

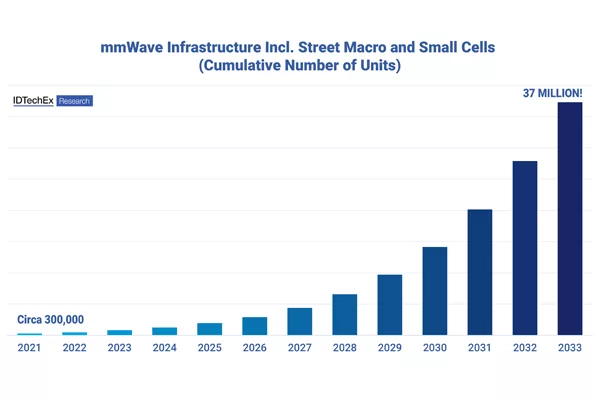

This article from IDTechEx offers an overview of the current deployment status and application focus of mmWave technology in key countries such as China, Japan, South Korea, the U.S. and the E.U. It provides insights into the specific areas where mmWave is being utilized and summarizes the development of the mmWave applications as well as the remaining challenges. These findings are based on IDTechEx’s latest 5G report: “5G Market 2023-2033: Technology, Trends, Forecasts, Players.”

In the U.S.:

The U.S. brings mmWave to consumers the earliest. Verizon, AT&T and T-Mobile have all commercialized mmWave service to improve network capacity and speed in congested urban hot zones or some campus networks, with Verizon leading the way and touting its performance. The use of mmWave technology in the U.S. has also expanded beyond urban areas, with some operators leveraging it for fixed wireless access in rural areas. Additionally, the country has seen significant progress in the development of mmWave consumer devices, with several smartphones and other devices supporting the technology.

Having said that, after the release of mid-band spectrum to operators in early 2021, there was a shift in deployment strategies among telecom operators in the U.S. – operators quickly changed course. They began prioritizing mid-band for their 5G deployments. Even Verizon shifted their attention to mid-band. This change in focus highlights the importance of mid-band spectrum for 5G development in the U.S., and the trend toward mid-band rollout is expected to continue in the coming years.

In China:

China's adoption of 5G technology is on a steady rise, with about one-third of its mobile users already using 5G as of the end of 2022, which is a 10.6 percent increase from the previous year. The 5G penetration rate in China is predicted to exceed 50 percent by 2024. It's important to note that the majority of 5G deployment in China is based on mid-band technology, which strikes a balance between speed and coverage, making it a more practical option for widespread deployment. According to IDTechEx, China leads the global 5G mid-band deployment with over 68 percent of the market share. mmWave, on the other hand, while several trials have been ongoing since 2019 to lay the groundwork for future mmWave deployment, this technology has yet to be commercialized in the country.

Currently, China is testing standalone frequency range 2 (26 GHz) only network type for mmWave, primarily focusing on congested network hotspot venues. However, there’s no doubt that the use cases for mmWave will be extended to industrial enterprises’ use cases, particularly in factories. Indeed, China's 5G strategy has always focused on industrial use cases, which is likely to continue in the future.

In South Korea:

Despite being the first country to launch 5G (on mid-band) commercially, South Korea's progress on mmWave deployment has been slow, even though the government has been releasing mmWave spectrum to operators early on. When the government allocated the 28 GHz band, it required each operator to build 15,000 base stations, but the installation rate has only been slightly over 10 percent. Given this sluggish development, the Ministry of Science and Information and Communication Technology of South Korea announced the cancellation of the 28 GHz band frequency allocation for operators KT and LG U+ on November 18, 2022. Furthermore, SKT's 28 GHz mmWave usage period was shortened to only six months. If the operators cannot construct 15,000 28 GHz 5G base station equipment by the end of May, their 28 GHz spectrum license will also be revoked. This underscores the government's emphasis on expediting the deployment of 5G mmWave infrastructure in the country.

In Japan:

The major telecom operators in Japan, namely NTT DOCOMO, KDDI, Softbank and Rakuten have introduced the mmWave 28 GHz band for their 5G networks and have already set up over 20,000 base stations. However, it's worth noting that mid-band remains the primary frequency band for large-scale coverage, while mmWave is used to enhance network capacity in areas with high traffic.

In Europe:

Although several countries have recently made mmWave spectrum available in Europe, the adoption of mmWave technology for 5G development has been the slowest among the five regions. Additionally, the penetration rate of mmWave consumer devices in the region is also the lowest, currently below 1 percent. Among European countries, Italy has emerged as a leader in bringing 5G to consumers through the promotion of mmWave for fixed wireless access. Other European countries are also making progress, with Telefonica showcasing 5G mmWave at the MWC 2023 event in Barcelona. Despite bringing mmWave to consumers, countries like Germany have dedicated their 26 GHz band for private network use cases. Deutsche Telekom recently announced at the MWC 2023 event that it plans to introduce standalone mmWave technology for 5G campus networks that offer high capacity and low latency use cases in the future. The company highlighted a clear demand for high uplink capacity and low latency in 5G enterprise connectivity.

To summarize, right now IDTechEx sees 5G mmWave primarily used for three use cases: indoor/outdoor congested network hot zones, fixed wireless access and indoor enterprise.

Hotspots such as stadiums, transportation hubs and congested areas require high-bandwidth connectivity for both indoor and outdoor users. This deployment type is common for mmWave in all countries with commercialized 5G. However, monetizing this enhanced connectivity remains an issue for operators. Increasing revenue from consumers upgrading from 4G to 5G has been challenging, and doubts remain about the feasibility of selling 5G mmWave passes for events. Additionally, users must have compatible handsets, and the device ecosystem is not yet mature in many countries. Finally, the experience needs to be exceptional for consumers to justify upgrading their devices for occasional events.

Fixed Wireless Access (FWA) provides wireless internet access to homes and businesses, offering faster deployment times, lower costs and greater flexibility compared to fiber. Last year, Ericsson and Digital Nasional Berhad achieved a record of connectivity up to 1 Gbps at distances of 11.2 km (using mmWave) in line-of-sight scenarios in Malaysia. FWA is therefore promoted by telecom operators as an ideal solution for remote or rural areas and places where laying fiber is difficult. For example, an Indian telecom operator Reliance Jio aims to ultimately connect 100 million locations with its FWA. However, the current bottleneck lies in the cost of customer premises equipment, which is currently around US$200 to US$300 per unit, making it unaffordable for most consumers in targeted emerging markets.

We've all heard about introducing mmWave private networks to indoor enterprises such as factories. According to IDTechEx's conversations with several industry leaders, mmWave technology will be selected only for mission-critical applications, such as robots with high-definition cameras in the production line that need to upload videos/photos quickly. Furthermore, an open line-of-sight setting is required for mmWave. To IDTechEx’s best knowledge, sub-6 GHz is the most preferred choice for many smart factories embracing 5G technology when compared to mmWave. The proportion of enterprise network deployment between sub-6 GHz and mmWave in such settings is projected to be around 80 to 90 percent versus 10 to 20 percent, respectively, at least in the next five to six years.

To achieve mass deployment of mmWave technology, challenges such as high prices, limited device ecosystem and lack of strong applications need to be addressed. However, regulatory considerations, spectrum availability and competition from other wireless technologies can also impact its growth and success. Efforts should continue to focus on lowering costs, expanding the device ecosystem, and investing in R&D for compelling applications.