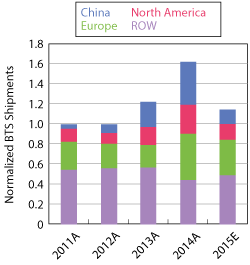

Figure 1 Trend in base station shipments by region, normalized to 2011. 2015 shipments are estimated. Source: EJL Wireless.

Wireless base station equipment shipments at the end of 2014 were supposed to accelerate to an even higher amount in 2015. However by the fourth quarter of 2014, demand was softening in China against all logic. Demand was supposed to increase due to China Mobile’s continued deployment of its TDD-LTE network while China Unicom and China Telecom were to ramp deployment of their FDD-LTE networks.

By last year’s Mobile World Congress (2015), EJL Wireless Research was seeing signs of a major anomaly within the industry, one that was not obvious. End market demand was completely uncorrelated to wireless industry financial conditions. Lead times were no longer stretched to the max, no bookings were doubled or tripled and no more orders were expedited. In some cases, orders were pushed out one quarter; in other cases, orders were cancelled. The party in China was over. We believe that a perfect storm of events occurred in China, beginning in the fourth quarter of 2014, that ultimately led to the widescale corruption and grafting probe by the Chinese government, one that impacted demand in the telecom market (see Figure 1).

This demand has not disappeared; it has merely been pushed out by one year. Our expectations are for wireless equipment demand in 2016 to pick up, with China leading the way. India may still support demand for TDD- and FDD-LTE, as operators continue deployment of their networks. Europe is in a holding pattern waiting for LTE demand to increase to a level where current coverage at 800 MHz (Band 20) is near capacity and the next overlay for capacity at 2600 MHz (Band 7) is required.

The strength that North America has supported from 2012 to 2014 is no longer there. North America is facing a new reality of wireless capital expenditures. The FCC’s auction 97 for AWS-3 spectrum (G, H, I and J blocks of paired spectrum and A1 and B1 blocks of unpaired spectrum in the 2100 MHz frequency band) essentially broke the bank of North American carriers. Gross bids of $44.9 billion forced tier-one operators such as AT&T and Verizon to find alternative ways to fund their spectrum purchases. With LTE coverage deployments at 700 MHz (Bands 13 and 17) essentially completed, focus in 2014 had shifted to adding capacity using the higher frequency bands, such as 1900 MHz (Bands 2 and 25) and 2100 MHz (Band 4), along with the introduction of 3GPP release 10 LTE-A features such as carrier aggregation.

IT’S THE SPECTRUM, STUPID

The wireless game is driven by spectrum. That is the bottom line. Nothing else matters to the mobile operator. There can never be too much spectrum. However, acquiring new spectrum for mobile operators results in a substantial financial impact at the initial stages of the acquisition: a government sponsored auction, then the implementation and deployment of new equipment for the new spectrum.

Germany recently auctioned a subset of 1500 MHz spectrum (Band 32) for supplemental downlink (SDL) with the U.K. slated to follow in 2016. Latin America and Asia Pacific are in the midst of auctioning APT 700 MHz (Band 28) “digital dividend” spectrum. In Europe, there is the potential for a digital dividend II (703 to 733 MHz and 758 to 788 MHz), which is a subset of Band 28. (Band 20 at 800 MHz was deemed the original digital dividend spectrum for Europe.) The repurposing of legacy WiMAX spectrum (3.4 to 3.7 GHz) to TDD-LTE technology allows for more wireless equipment to be sold. The promise of 5G is set to be the millimeter wave industry’s ultimate fantasy and dream come true.

How does new spectrum impact the wireless equipment ecosystem? Without new spectrum becoming available, the wireless equipment industry would stagnate and stall. There would not be any growth at all. Given these regional and spectrum constraints, how will the various segments of the wireless infrastructure market fare?

BTS ANTENNAS

Five major events could trigger a mobile operator to upgrade their antenna mast systems:

- New technology (e.g., LTE)

- New spectrum

- Updating radio transceiver MIMO capability to two transmit and two receive (2T2R), 2T4R, 4T4R, 4T8R or 8T8R

- Site acquisition issues

- Migration to semi-active or active beam forming antennas.

Each of these causes potentially complex issues to be resolved by the mobile operator, and each macrocell site may have a different issue. As an example, in North America the current frequency bands for LTE are

- 700 MHz (Bands 12, 13 and 17)

- 800 and 850 MHz (Bands 5 and 26)

- 1900 MHz (Bands 2 and 25)

- 2100 MHz (Band 4).

The eventual deployment of AWS-3 spectrum will force mobile operators to replace existing AWS-1 remote radio units (RRU) with updated ones that may support 2T4R or 4T4R configurations, as well as the expansion of the frequency band to support the AWS-3 spectrum. We believe that the majority of Band 4 RRUs will be upgraded from 2T2R to 2T4R, requiring two additional ports on the antenna.

The potential impact of the upcoming 600 MHz auction in 2016 will again force mobile operators to deploy a separate antenna panel to support this specific band, due to the size of the dipole columns needed at this lower frequency range.

For a worst case scenario, where each band (700, 850, 1900 and 2100 MHz) supports a 2T4R configuration without diplexing low or high bands together and not counting for different electrical tilts for different types of wireless services, a single sector panel antenna would need 16 ports and potentially eight dipole columns using a cross polarization (xpol) type of dipole array. One simple issue relating to the realities of panel antennas is that weight and wind load play a significant factor in their deployments. The width of the panel antenna is typically kept to a maximum of 400 mm to minimize wind loading. It is very difficult to get approval to mount a door on a tower; however, we have seen instances of very wide antennas being deployed on rooftops where the wind load is offset by supporting structures.

Figure 2 Multi-band antenna faceplate, showing four low band (red outline) and eight high band (blue outline) ports integrated into a single housing. Source: Commscope.

Figure 3 Ericsson microcells for Bands 2 and 4, deployed on a streetlight in San Francisco, Calif. Source: EJL Wireless.

We estimate that BTS macrocell antenna shipments increased 37 percent year-over-year in 2014, and 2015 shipments will show a decline of 30 percent in unit volume due to the weakness in China and North America. The market for TDD-LTE antennas (e.g., 8+1 ports) was approximately 24 percent of overall shipments in 2014. We also estimate that FDD-LTE four-port antennas were the largest product segment, followed by two-port and six-port antennas. The semi-active/active antenna segment was only 2 percent in 2014.

We believe that there are two major trends over the next several years for macrocell antennas: higher and higher port count to 8, 10, 12 and 14 (see Figure 2) and migration to 4.3/10 mini-DIN connector ports. While there may be some specific requirements for semi-active antennas (e.g., passive antennas with RRUs), we believe that these may be due to site acquisition issues and not necessarily because of performance improvements.

OUTDOOR SMALL CELLS

The North American market has seen a complete shift in strategy towards small cells, as AT&T Wireless shifted its position from deploying 40,000 small cells to no longer focusing on them. Conversely, Verizon Wireless has stated it will spend $500 million on small cells in certain markets (see Figure 3).

With Verizon, the advent of outdoor small cell deployments is finally seeing some larger scale demand. There is currently a 400+ “small cell” deployment ongoing in San Francisco, Calif.; however, this questions the definition of a small cell. We believe that stand-alone small cells have the baseband processing modem integrated with the radio transceiver, with either a direct Iub connection to the core network or an Iuh connection to a gateway controller. Otherwise, we classify “small cells” deployed with a fiber fronthaul link as an outdoor distributed antenna system (oDAS) remote radio node — not a small cell. We believe that the San Francisco deployment is a hybrid of both traditional small cells and oDAS radio nodes.

In Europe, announcements from Vodafone U.K. and advertising giant JCDecaux are paving the way for outdoor small cell deployments. Unlike the North American market, we believe that mobile operators in Europe will not share infrastructure and will deploy single operator small cell solutions, not oDAS radio nodes. The acquisition of sites and street furniture for small cells has been one of the largest impediments for deploying outdoor small cells, with backhaul also being a large issue. With the ability to use JCDecaux street furniture across Europe, the site acquisition issue may have been solved for mobile operators.

IN-BUILDING WIRELESS

The term in-building wireless (IBW) encompasses many different solutions and technologies and is confusing for the wireless industry. We classify the following solutions as in-building wireless:

- BTS OEM picocells

- Passive distributed antenna systems (p-DAS)

- Active analog distributed antenna systems (aa-DAS)

- Active digital distributed antenna systems (ad-DAS)

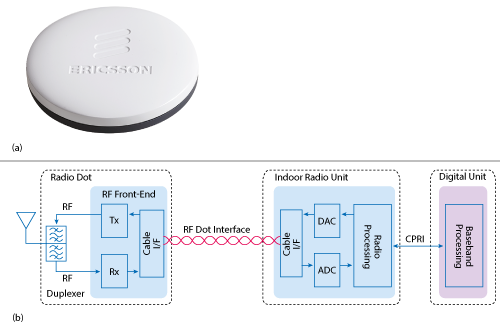

- BTS OEM solutions such as Ericsson’s Radio Dot (shown in Figure 4) or Huawei’s LampSite

- Third party small cells with controller gateways (e.g., SpiderCloud or equipment from CommScope).

Figure 4 Ericsson’s indoor small cell solution connects multiple RF front-ends (a) to an indoor radio unit (IRU), with multiple IRUs connected to a single digital unit for baseband processing (b). Source: Ericsson.

The North American market has historically led the global IBW industry, given the large sporting venues, airports and convention centers located within the U.S., with aa-DAS the predominant technology used. However, we see other regions such as Asia Pacific and Europe adopting single operator solutions offered by BTS OEMs and third party small cells, since the neutral host model in these regions is not as defined as it is in North America.

Wi-Fi LAA/LTE-U

The use of unlicensed spectrum at 5.8 GHz through the license assisted access (LAA) specifications in 3GPP release 13 will allow mobile operators to leverage an 80 MHz chunk of spectrum, essentially for free. This is the equivalent of offering mobile operators billions of dollars of free spectrum. Using licensed LTE spectrum for signaling, the unlicensed 5.8 GHz spectrum may be used to transmit and receive LTE signals from user equipment (UE). Incumbent Wi-Fi proponents argue that LAA technology will essentially block their Wi-Fi signals. We do not believe that this will be the case, as the LTE transmissions will be subject to the same restrictions as any other Wi-Fi access point deployed within the same area. We believe that LAA will be deployed in both in building and outdoor use cases globally, beginning in 2016.

2016 OUTLOOK

Data usage and spectrum drive the wireless industry. Auctions for spectrum worldwide will continue to fuel the industry while LTE/LTE-A adoption and usage continue to increase globally.

The demand for LTE in China will be the key barometer for the industry. The partnership agreement between China Telecom and China Unicom following swirling rumors of operator consolidation may dampen the outlook and shift the industry’s focus to India. We expect global base station demand to be flat to up if China comes back or flat to down if China fails to meet expectations.

Wi-Fi calling and LAA/LTE-U will be a hot topic for 2016 as mobile operators attempt to offload voice and data traffic from LTE and W-CDMA networks to the unlicensed band at 5.8 GHz. Mobile operator carrier grade Wi-Fi deployments will likely drive demand worldwide should operators quickly adopt LTE-A to access these features.