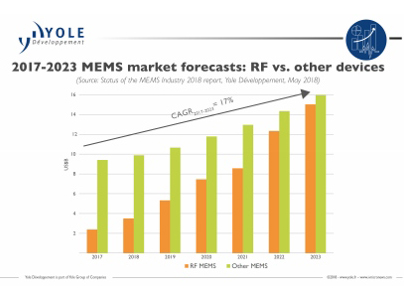

“MEMS market will experience a 17.5 percent growth in value between 2018 and 2023, to reach US$ 31 billion at the end of the period,” asserts Dr. Eric Mounier, principal analyst, MEMS & Photonics, at Yole Développement. “The consumer market segment is showing the biggest share, with more than 50 percent. The good news is that almost all MEMS devices will contribute to this growth.” However, the RF industry is still playing a key role in the MEMS industry development. Excluding RF, the MEMS market will grow at 9 percent over 2018 to 2023. With RF MEMS devices, CAGR reaches 17.5 percent during the same period. Driven by the complexities associated with the move to 5G and the higher number of bands it brings, there is an increasing demand for RF filters in 4G/5G, making RF MEMS (mainly BAW filters) the largest-growing MEMS segment.

Yole releases today its annual MEMS technology & market analysis: Status of the MEMS Industry. This 2018 edition presents the MEMS device market along with key industry changes and trends. The market research and strategy consulting company is following the MEMS industry for a while, tracking more than 200 applications and 300 MEMS companies. This report is a significant combination all of these applications into more than 15 major MEMS devices. This 15th version includes: global macro economical megatrends and their impact on MEMS and sensors business–MEMS and sensors market forecast–manufacturers rankings–analysis by device and application.

Amongst the numerous existing MEMS devices, inkjet heads will grow, with the consumer market representing more than 70 percent of printhead market demand. This market recorded its first signs of recovery in the first half of 2017, a trend confirmed in the second half of the year. This recovery was noticed both in disposable and fixed printheads. Most consumer players show discernable growth: for example, HP has recorded a 2 percent growth in consumer printer revenue since 2016, and Canon has confirmed a progression in sales for inkjet printers, with strong demand in Asia.

Numerous pressure sensor applications also contribute to market expansion. Indeed, it is interesting to see that, although it is one of the oldest MEMS technologies, pressure sensor keeps growing. In automotive, pressure sensors have the highest number of applications, with many advantages such resistance to toxic exhaust gas and harsh environments, higher accuracy and the development of intelligent tires that deliver more information on tire status (especially for future autonomous cars). For consumer, mobiles and smartphones still account for 90 percent of pressure sensor sales, and cost reduction is the priority vs. size reduction because size is already very small. Although there are no big “killer” applications expected in the future, new applications are emerging: smart homes, electronic cigarette, drones and wearables, to name several.

Then after, are coming the MEMS microphones. Such MEMS components have been in the spotlight for a long time and have expressed one of the highest CAGRs of any MEMS technology over the last five years. “In the range of US$105 million in 2008, the MEMS microphone market was worth US$402 million in 2012 and reached the US$1 billion milestone in 2016”, asserts Guillaume Girardin, director of the Photonics, Sensing and Display division at Yole. “Currently, almost 4.5 billion units are shipped annually. The main application is mobile phones, which comprise 85 percent of shipment volumes, in a consumer market that makes up 98 percent of the total shipment volume. Tablets and PCs/laptops take second and third place, with 5 and 3.2 percent of total shipment volumes, respectively.”

Step by step, the uncooled IR imager market keeps growing. This is due to a continuous price decrease over the last few years stemming from new technologies such as WLP and silicon lenses, as well as increasing acceptance from customers. As prices continue falling, we believe the market for uncooled IR imaging technology will continue finding new applications in the coming years. More results will be detailed during the 3rd Executive Infrared Imaging Forum, powered by Yole and taking place on September 7 in Shenzhen, China.

All MEMS market segments including inertial, optical MEMS, microfluidics, new micro components and more are deeply analyzed in Yole’s annual MEMS report, Status of the MEMS Industry.

In this new edition, Yole’s team is also analyzing the market positioning of the MEMS device manufacturers and their annual revenue. What is the status of the 2017 Top MEMS manufacturers?

- In 2017, the biggest surprise was Broadcom becoming the #1 MEMS player. As growth continues for RF, driven by an increasing number of filters/phones and by the front-end module’s increasing value, it is likely that RF players will still dominate the top 2018 rankings.

- In parallel, most MEMS players showed positive growth in 2016 to 2017. Established players, Robert Bosch, STMicroelectronics and HP were “shaken” by Broadcom’s growth but still performed well. For example, the German leader, Robert Bosch enjoyed growth of approximately US$100 million. Inkjet heads players also had a good overall performance compared to previous years. In addition, the company, SiTime displayed the most impressive growth, exceeding 100 percent. Other MEMS players posting significant growth are: FormFactor, benefiting from the semiconductor business’s excellent health; and ULIS, with uncooled IR imaging still growing annually into multiple applications including consumer–thermography, firefighting, night vision, smartphones, drones and military.

In 2016, the top 30 MEMS players totaled more than US$9,238 million. In 2017, that number increased to US$9,881 million.

Further results, extracted from Yole’s technology & market analyses will be presented by its team, during key conferences and trade shows all year long.